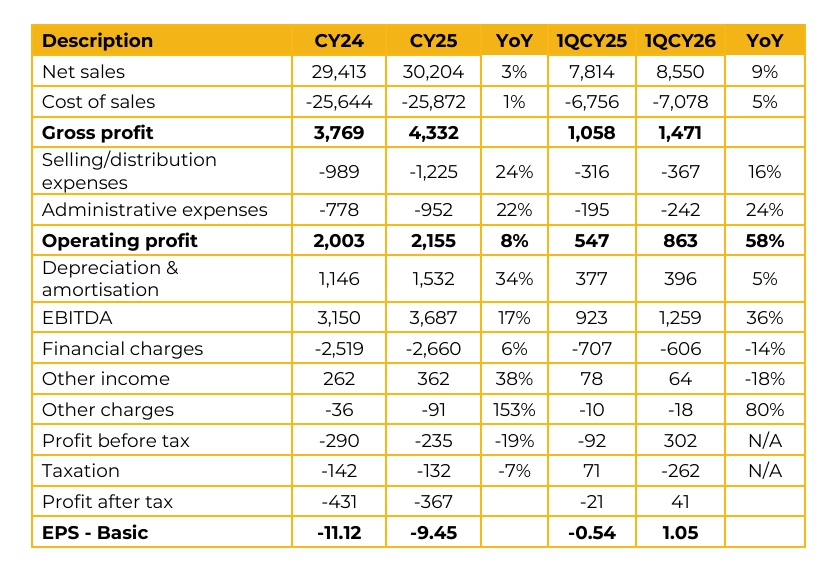

Tri-Pack Films Limited (TRIPF) reported loss per share of PKR 9.45 for CY25, compared to PKR 11.12 in CY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 1.05, compared to loss per share of PKR 0.54 in the same period last year (SPLY). The company successfully commissioned Line 5, which is the latest and largest expansion in its BOPP segment. In addition, a new tape machine has been installed to facilitate the production of specialized adhesive tapes, further diversifying the product portfolio.

Management highlighted that Pakistan’s current BOPP demand stands at approximately 80,000 tons, whereas total installed capacity has increased to 161,000 tons following the entry of new players.

This overcapacity is expected to persist over the medium term. Tri-Pack continues to maintain a dominant market share of 46% in the local market, while typically operating with an inventory of around 30 days. In response to a 44% increase in gas prices, the company is transitioning approximately 40% of its power requirements to K Electric, with the system expected to become operational by May. Currently, the weighted average cost of electricity stands at PKR 56/ unit however, management expects a meaningful reduction of up to PKR 20/unit once K-Electric and BESS are fully integrated. To manage excess capacity, the company has expanded its export footprint to 20 countries, including the USA, Canada, Europe, and the Gulf region.

Exports currently account for 17% of total production, with management targeting an increase to 25%–30%. On the procurement side, due to ongoing regional disruptions, the company is planning to diversify its raw material sourcing beyond traditional Gulf suppliers toward China, reducing supply chain concentration risk. From a regulatory perspective, the import duty structure remains favorable for local producers, with finished film imports subject to 15% customs duty plus 2% additional duty, while raw materials are charged only 2% additional customs duty. Lastly, management noted that while the company recorded some inventory gains due to fluctuations in raw material prices, these were largely offset by the increase in gas levies, which have risen from PKR 800 to PKR 1,400 per unit, with a potential increase to PKR 2,500 going forward.

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.