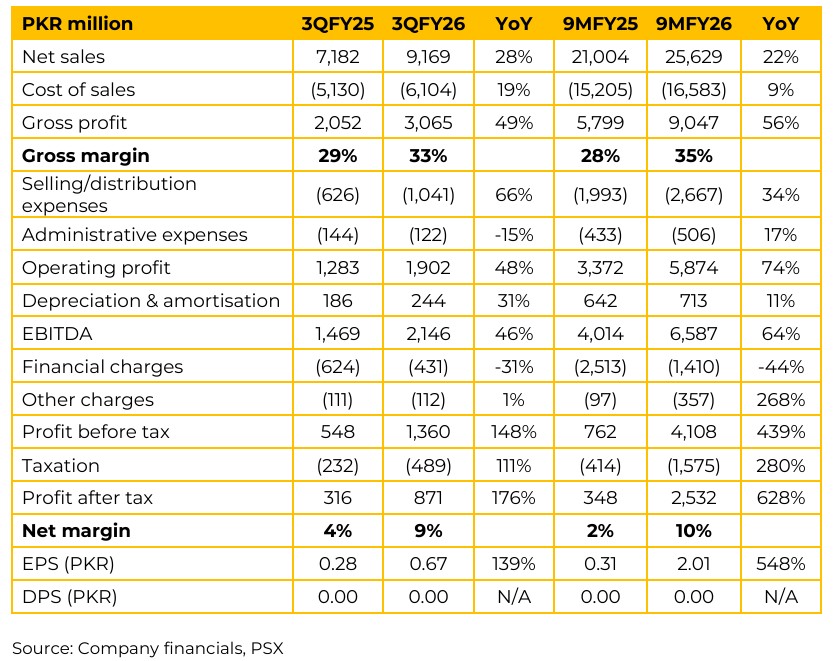

Power Cement Limited (POWER) reported earnings per share of PKR 2.01 for 9MFY26 (PMFY25: PKR 0.31). Meanwhile in 3QFY26, POWER reported EPS of PKR 0.67 (3QFY25: PKR 0.28). Total dispatches grew by 16% during 9MFY26. The sales mix currently stands at 54% local and 46% export. Local sales grew by 2%, while clinker exports saw a massive 61% increase. For 9MFY26, POWER achieved 100% capacity utilization on its new 7,700-ton line.

Total South industry capacity utilization stood at 86%, significantly higher than the North’s 54%. The company successfully reduced its cost per ton by approximately PKR 500 through energy efficiencies and fuel mix optimization. Power Cement is aggressively shifting away from grid dependency. Following the inauguration of a 7.5 MW wind turbine in May 2026, the energy mix is moving toward a 52/48 split between grid and renewable sources (Solar, Wind, and Waste Heat Recovery). The 7.5 MW wind project is a first-of-its-kind 20-year Power Purchase Agreement (PPA) where Power Cement buys electricity at a committed rate rather than owning the asset.

The company achieved a 25% substitution rate using agricultural waste (rice husks, wheat, cow dung) to replace imported coal. They aim to maintain a 20-25% substitution rate going forward. Management noted a silver lining where Pakistan gained market share in Africa and the Middle East because Egypt and Algeria exited these markets to serve their own neighboring regions. Major markets now include East/West Africa, Kuwait, and Bangladesh.

Current local retention prices are between PKR 16,350 and 16,550 per ton. Clinker export prices are currently $36 to $38 per ton. The company currently holds low-cost coal inventory that is expected to last through July. They aim to maintain a 45-to-60-day inventory of coal to buffer against supply shocks. Imported coal remains the primary fuel source, accounting for approximately 80% to 88% of the company’s fuel mix. Petcoke prices are currently aligned with coal, ranging between $110 and $115 per ton. It is primarily imported from the USA, which involves long-distance shipping. Petcoke has a high heating value (Gross Calorific Value or GCV) of 7,500 kcal/kg. It currently makes up approximately 7% to 10% of the fuel mix.

Alternative fuel is significantly more cost-effective, with a GCV-based price that is approximately 40% lower than coal. The GCV of alternate fuel is between 3,500 and 4,000 kcal/kg, compared to coal’s average GCV of 6,000 kcal/kg. It currently averages about 10% of the total fuel mix.

Before the full integration of the new wind project, the average power cost was approximately PKR 22 to PKR 24 per unit. With the wind project now online, management expects the blended average cost to drop to between PKR 20 and PKR 22 per unit. Going forward, management expects domestic demand to grow by 5% to 7% next year, historically tracking at 1.5x to 2x Pakistan’s GDP growth.

Payments on mark-up for loans from associated companies are at the company’s discretion and will only be prioritized after meeting long term loan obligations and CAPEX requirements. Management stated there are currently no proposals on the table regarding an acquisition by a larger player.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.