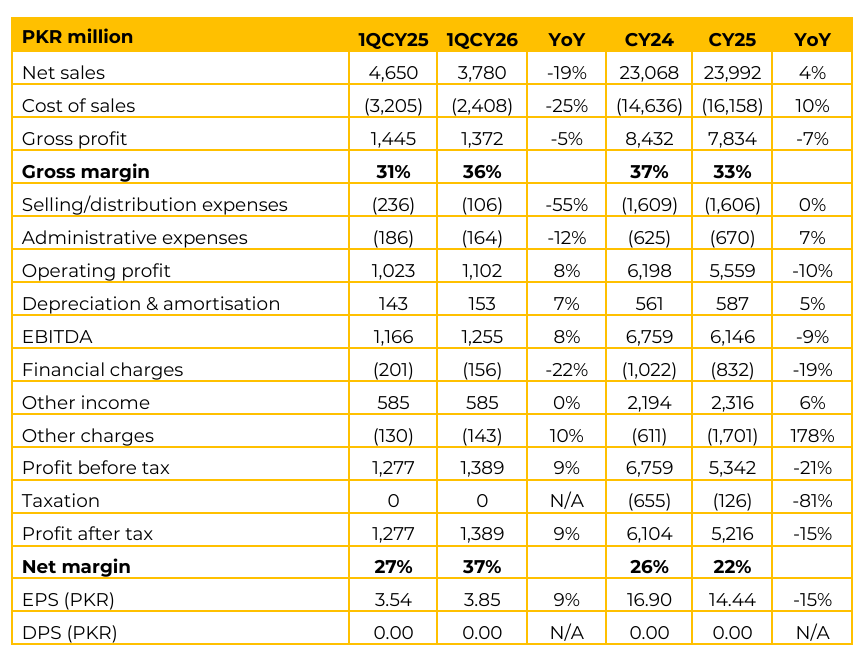

PABC reported earnings per share of PKR 3.85 in 1QCY26 (1QCY25: PKR 3.54). In CY25, EPS stood at PKR 14.44 (CY24: PKR 16.90). In CY25, revenue reached PKR 23.99 billion, a 4% increase from the previous year, representing the highest sales figure in the company’s history.

Local sales volume grew by 12%, while export volumes declined by 10% due to border disruptions. Exports now make up 62% of total revenue, down from 67% in CY24.

A PKR 1.1 billion impairment allowance was recorded for slow moving stock (approximately 80% of value) that reached expiry due to the Afghanistan border closure. Capacity utilization stood at 52% for the year, a decline from CY24 levels primarily due to the ongoing Torkham border disruption that began in October 2025.

The board has approved a proposed project for a can plant in Afghanistan with a rated capacity of 1.3 billion cans (subject to regulatory approvals) and an estimated budget of $110 million.

The timeline remains uncertain pending financial close. Due to regional geopolitical challenges, PABC is targeting alternate markets. Bangladesh is being targeted more aggressively for higher market share. The company is also exploring alternate routes via Iran-Pakistan corridor to reach Central Asian countries.

Moreover, the company is also focusing increasing the domestic “can” share of the beverage market, which currently remains small compared to global averages. Going forward, the management expects domestic demand to grow by 10-15% if political and economic stability persists.

Management stated that Super Tax is currently not applicable due to their operation in a special economic zone. The company’s tax holiday is to expire on 30th September 2027.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.