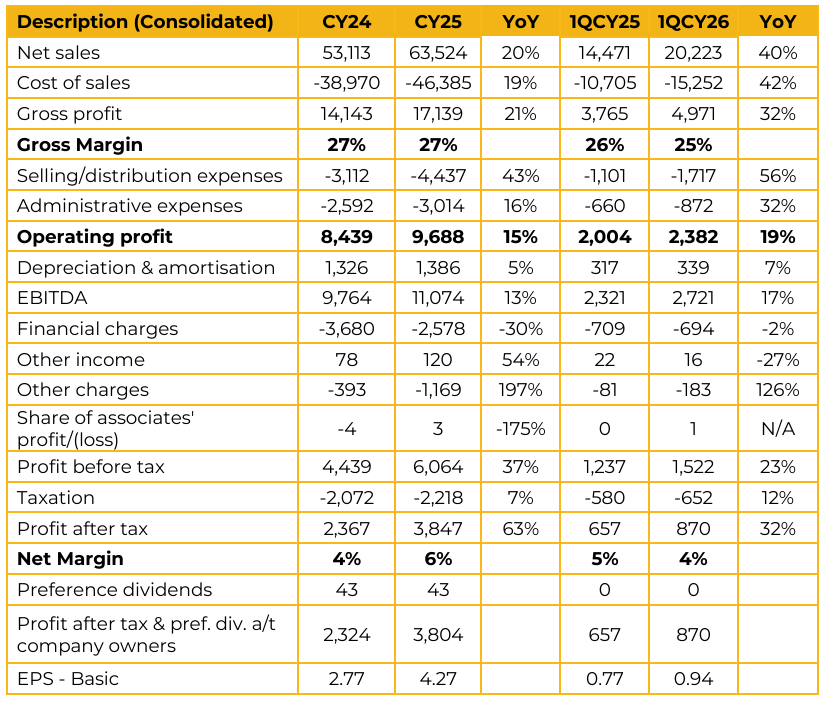

Pak Elektron Limited (PAEL) reported earnings per share of PKR 4.27 for CY25, compared to earnings per share of PKR 2.77 in FY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 0.94, compared to earnings per share of PKR 0.77 in the same period last year (SPLY). In the appliances division, management highlighted significant growth potential driven by low regional penetration levels.

Refrigerator penetration currently stands at 51%, while air conditioner penetration remains considerably lower at 15%, indicating substantial room for expansion. PEL maintains a dominant position in the power equipment segment, holding an estimated market share of approximately 80% in power transformers. The company also commands market shares of 25% in switchgears segment, energy meters 18%, and distribution transformers 17%. PEL has already achieved exports of US$17.5mn as of April 2026.

Management reiterated its export target of US$20mn for FY26, while also highlighting an ambitious target of US$50mn for FY27. Management clarified that the previously discussed US$100mn export figure was based on preliminary negotiations and customer inquiries. In contrast, the current FY26 export target of US$20mn is supported by confirmed orders. Rising material costs have been passed on to consumers through recent price increases in refrigerators and ACs.

Although supply chain disruptions continue to persist, the company is maintaining elevated inventory levels to mitigate potential shortages. Management noted that most large scale smart meter tenders in Pakistan are funded by international institutions such as the World Bank and IFC. These projects typically involve stringent financial and operational pre qualification criteria, which local manufacturers currently struggle to meet, resulting in Chinese firms securing the majority of such contracts. PEL is actively engaging with the relevant ministry to advocate for more accessible qualification criteria and may explore a foreign joint venture partnership in the future.

PEL has now obtained full UL certification, enabling the company to supply products to local US utilities and large scale manufacturers. On the tariff front, management believes the company enjoys a relative advantage over regional competitors including China, India, and Bangladesh. Additionally, most US contracts are structured on a CIF basis, whereby the customer bears the impact of any import duties.

TVs remain a relatively low priority and lower margin category for PEL. Management indicated that the segment primarily serves to complete the company’s consumer product package during the wedding season, while also supporting dealer engagement during the off peak season. PEL has recently incurred capex of approximately PKR 800mn–1bn on plant, machinery, and buildings to support export operations.

Management believes the company’s existing manufacturing capacity is sufficient to meet near term demand requirements without the need for a major expansion. While management did not disclose product wise profitability, it highlighted that export margins are approximately 10% higher than those generated in the local market. Additionally, management guided towards sustaining its growth trajectory in FY27, targeting revenue growth of over 20% YoY.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.