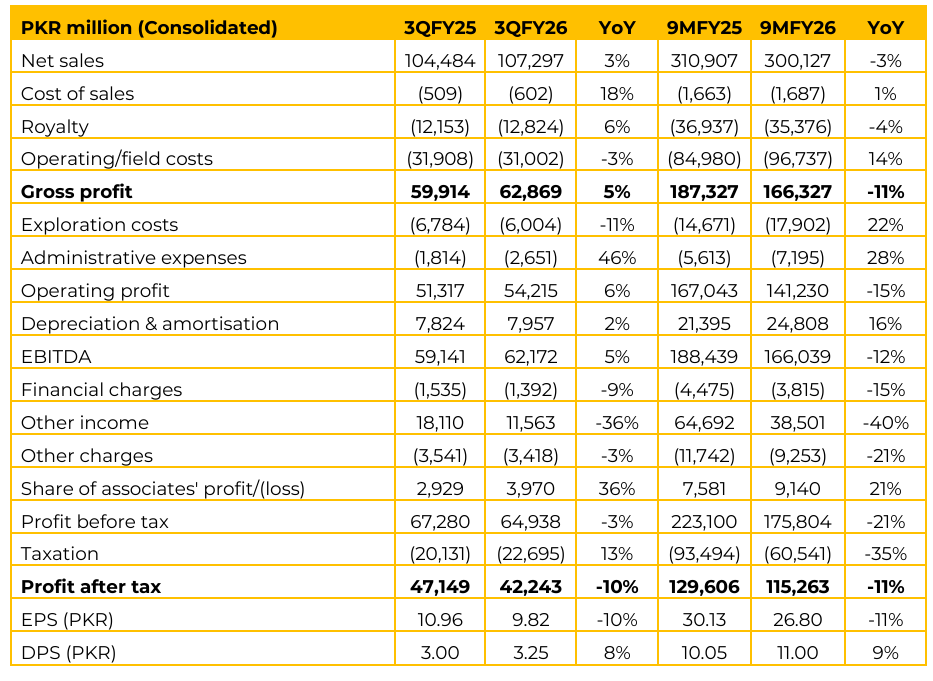

OGDC reported consolidated earnings per share of PKR 9.82 in 3QFY26 (3QFY25: PKR 10.96). In 9MFY26, EPS stood at PKR 26.80 (9MFY25: PKR 30.13).

Management noted that OGDC has achieved a 6.5-year high in oil production, currently producing approximately 40,341 barrels per day. This achievement comes despite historical declines in various fields. The Baragzai field was injected in April. While initially announced as a 5,300 bpd discovery, the first try yielded 6,000+ bpd and 18 mmscf of gas.

The company has significantly improved drilling times in South Pakistan, completing multiple wells in 12 to 20 days. This is attributed to state-of-the-art, GPS-directed seismic systems that are currently unique to OGDC in the Pakistani market. The Reserve Replacement Ratio for the first nine months stands at 153%.

For owned and operated portfolios, this ratio is even higher at 240%. The total estimated size of the Baragzai discovery is over 100 million barrels of oil equivalent. OGDC plans to ramp up production to 22,000–25,000 bpd over the next 2 to 2.5 years by utilizing existing facilities at Manzalai before expanding in 2028.

A “Production Optimization 2.0” drive is underway. Since July 2023, optimization efforts have added approximately 11,700 bpd to the total production. Management is targeting a production level of 48,000 bpd by December, assuming no significant production curtailment occurs.

Total production capacity is higher than actual output. Current curtailment stands at approximately 2,671 bpd of oil and 53 mmscf of gas. Production at Bettani is currently constrained by SNGPL pipeline capacity. This is viewed as a 6 to 12-month issue that requires pipeline enhancement to absorb higher pressures from new discoveries. Curtailment due to LNG line pressure has decreased significantly compared to earlier in the year

A high-prospectivity well in KP is near completion. Management noted its value could be substantial, though it remains subject to exploration risks. On Reko Diq, development activity continues with civil works underway, while financing and partner-level discussions remain ongoing and sensitive.

There was a slight deterioration in receivables collection, which stood at 87% this quarter. This follows an anomalous previous quarter where a large PKR 24 billion settlement from Uch skewed the percentage higher. Approximately PKR 20 billion is currently owed from the Central Power Purchasing Agency (CPPA). However, collection in April was noted to be significantly better than the entire previous quarter combined.

Management highlighted continued uncertainty around the super tax, with assessments ongoing across 50+ Petroleum Concession Agreements (PCAs). Given procedural timelines, reversal of provisions appears unlikely in the near term, and management refrained from providing quantifiable guidance.

The windfall levy case remains sub judice, with no additional clarity provided. Overall, management’s stance suggests maintaining conservative assumptions until visibility improves. Going forward, substantial capital expenditure is expected for 2027 and 2028, remaining in a similar range to the current year.

On pricing, management reiterated that realized crude prices are based on physical delivery benchmarks (linked to a basket), with actual realizations typically at a discount to international benchmarks due to policy structures. Pricing dynamics vary by field, with some assets (e.g., Nashpa) benefiting from no price ceiling, while others are subject to windfall sharing or capped upside.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.