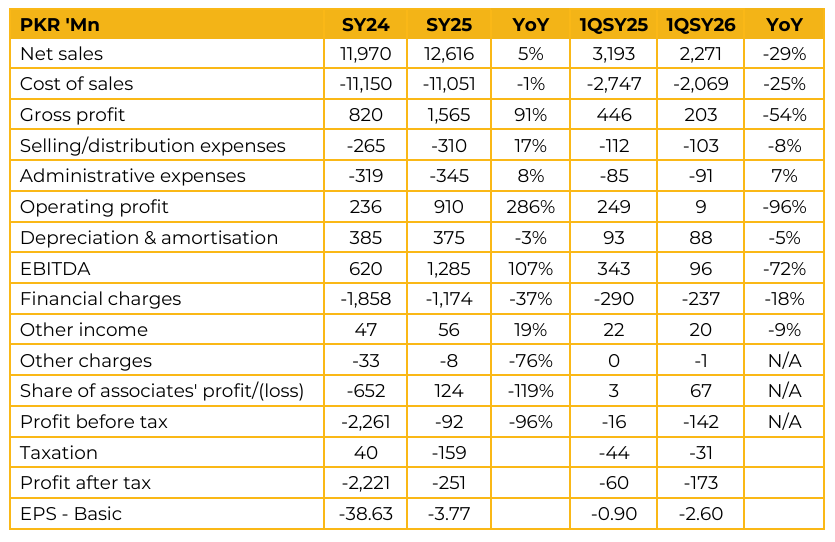

Mirpurkhas Sugar Mills Limited (MIRKS) reported loss per share of PKR 3.77 for SY25, compared to loss per share of PKR 38.63 in SY24. Furthermore, in 1QSY26, the company reported loss per share of PKR 2.60, compared to loss per share of PKR 0.90 in the same period last year (SPLY). National sugar production is projected at 6.8–7.0 million tons against estimated consumption of 6.3–6.4 million tons, resulting in a surplus of 0.5–0.7 million tons.

Management expects prices to remain range bound due to this surplus. Overall crushing declined in line with regional trends, while sucrose recovery rates in the South improved significantly to 10.29%. The crushing season began with sugarcane priced at PKR 425 per 40kg and has since increased to PKR 500–550 per 40kg. The prevailing ex-mill sugar price in the market is currently in the range of PKR 138–140 per kg.

The paper division faces intense competition from informal players. Production has increased from 32,000 tons to 43,000 tons compared to SPLY. The segment struggles to compete with unregulated suppliers who avoid the 18% sales tax, creating a pricing disadvantage for compliant corporate players. To improve cash flows and reduce reliance on the 60–70 day credit cycle in the local market, the company is exploring paper exports to the Middle East. The company’s Agro-Pulping Plant is expected to commence operations by April or May 2026.

Management intends to export surplus pulp, as the plant’s capacity exceeds internal consumption requirements. Management also noted that the historical cost advantage of generating internal power from bagasse is no longer in place. This follows the government’s reduction in industrial power tariffs for higher consumption slabs, bringing grid electricity prices closer to in-house generation costs.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.