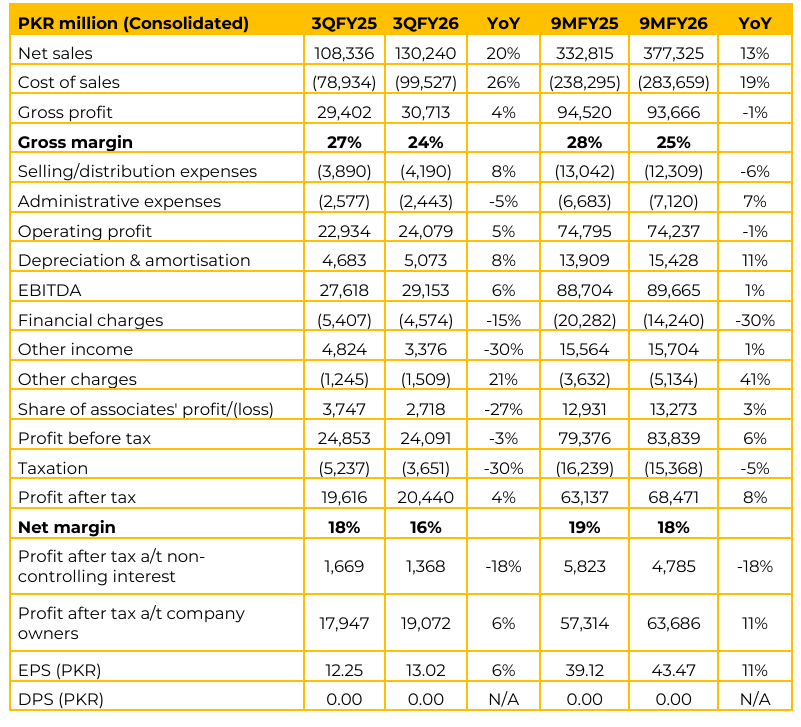

Lucky Cement Limited (LUCK) reported consolidated earnings per share of PKR 43.47 (standalone: PKR 39.12) for 9MFY26. Meanwhile in 3QFY26 LUCK reported EPS of PKR 13.02 (3QFY25: PKR 12.25). Domestic sales volume grew by 9% during the first nine months.

Management noted that growth would have reached double digits if not for price and cost escalations resulting from the Iran US war. Export volumes for the 9-month period stood at 2.3 million tons. Africa remains the primary destination, accounting for 74% of exports, with key markets including Cameroon, Madagascar, Kenya, and Ghana. The average local retention price for Q3 was PKR 15,500 per ton (up PKR 500 from the previous quarter).

Average export retention (clinker and cement) was approximately $40 per ton on an FOB basis. The company announced a 1.6 million tons per annum expansion at its Congo plant. This will be a fully integrated manufacturing facility, doubling the current capacity to meet growing market demand. LMC added the GAC brand to its portfolio alongside Kia and Peugeot. Four new models were recently rolled out, including a focus on the Electric Vehicle (EV) segment. A 15 MW solar project was added to the Karachi plant, bringing total solar capacity to 89.3 MW. Combined with wind and WHR, renewable sources now contribute 56–57% of the company’s energy mix. New technology at the Karachi plant allows for higher clinker production using less coal and enables the use of inferior quality (higher sulfur) coal, improving cost competitiveness.

Lucky Electric provided PKR 12 billion in dividends (two interim payments of PKR 6 billion) during the nine months, compared to PKR 6 billion in the same period last year. Consolidated margins were impacted by Lucky Core Industries (LCI), which faced competition from dumped soda ash and polyester products from China due to reduced duty rates. Additionally, Iraq operations saw a dip in Q3 due to geopolitical tensions affecting the local economy.

The average cost of coal (local and imported) is currently around PKR 40,000 per ton. The company maintains a 60-day coal inventory and a 30-to-45-day clinker inventory. Going forward, for FY27, management expects more modest domestic growth of approximately 5% as the economy absorbs the lag effects of inflation and interest rates. Lucky Electric currently uses 40–50% local coal and is expected to transition to 100% local coal by 1QFY27.

However, circular debt remains a risk to sustainable dividend payouts. The company is evaluating multiple privatization projects and other investment opportunities but has no immediate legal plans to restructure into a formal holding company. Management sees no further consolidation in the cement sector in near future.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose