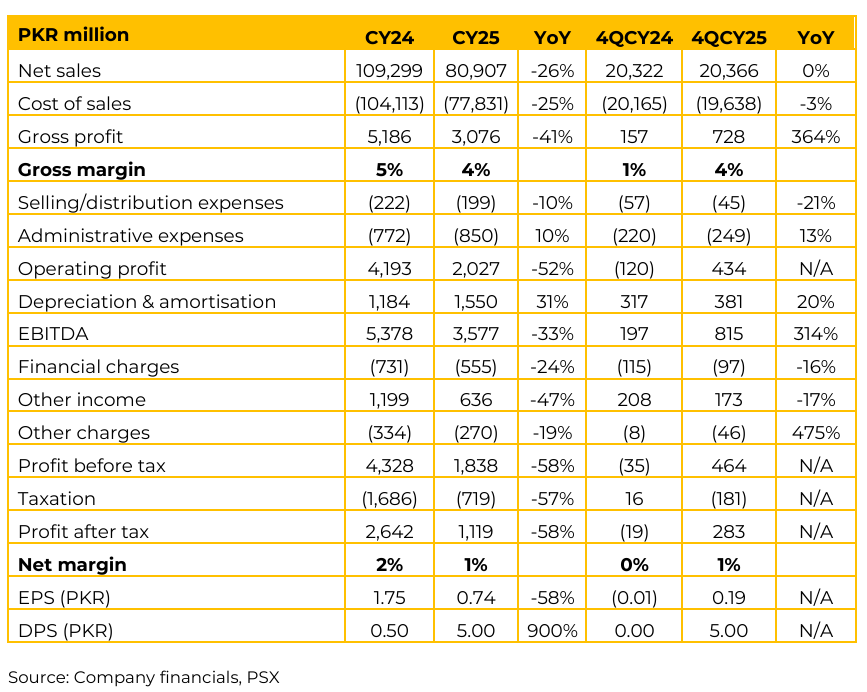

LOTCHEM has posted earnings per share of PKR 0.74 in CY25 (CY24: PKR 1.75). Moreover, in 4QFY25 the company marked an EPS of PKR 0.19 as compared to loss per share of PKR 0.01 in 4QCY24. The company is aiming to move toward 100% domestic captive customers by 2027, up from three of five major customers currently. This is supported by a ~9.5% anti-dumping duty (ADD) on Chinese PTA imports.

Management stated they do not intend to use the ADD to gain “windfall profits” but rather to ensure a level playing field. The company is methodically redesigning and rescoping hundreds of engineering and non-engineering contracts. A methodical review of hundreds of contracts is yielding 15–30% savings per contract, targeting a 25% (PKR 500 million) annualized reduction in fixed costs by the end of 2026. LOTCHEM targets a 40% total reduction in conversion costs by January 2028. As of March 2026, costs are already down 14% due to grid tariff reductions and operational changes. By switching from captive gas (44 rupees/unit) to the 220 KV grid and utilizing new government incremental consumption tariffs, costs have dropped to approximately 23–24 rupees per unit.

The Battery Energy Storage System has eliminated the need for continuous diesel backup, saving Rs 600 million annually. Solar power of 6.5 MW will be energized in April 2026, with an additional 15 MW planned by November 2026. Azeotropic Distillation project uses waste heat to generate power. Phase 1 (1QCY27) is expected to produce 6.5 MW and reduce conversion costs by 10%. Phase 2 (4QCY27) is expected to produce an additional 6 MW.

Total energy capex (including BESS and Solar) is estimated at Rs 2.5–2.8 billion, with paybacks of one year or less for most projects (two years for solar). A central component of Lotte’s growth strategy is the acquisition of EPCL to create a diversified integrated petrochemical platform.

Management highlighted that there is low correlation (0.3%) between PTA and PVC margins, providing a natural hedge against commodity cycles. PVC margins are showing signs of improvement. Notably, China’s decision to abolish its 16% export rebate on PVC (effective April 1, 2026) is expected to improve PVC margins by $70–75. EPCL is currently not connected to the grid and operates on captive power at 44 rupees/unit.

LOTCHEM possesses two 220 KV grid lines and a right-of-way to EPCL’s facility. Connecting EPCL to LOTCHEM’s grid could yield energy savings of PKR 6-8 billion annually. Estimated fixed cost savings of Rs 1–1.5 billion and improved cash flows via the adjustment of accumulated sales tax. LOTCHEM plans to utilize 50 acres of vacant land to build a “Renewables Park” (25 MW Solar and 16 MW Wind) to cater to the combined entity’s 68 MW power requirement.

The transaction is envisioned as all-equity. The Share Purchase Agreement (SPA) is expected within 45 days, with the acquisition potentially concluding by August 2026. Going forward, the management expects significant inventory gains driven by price jump of Paraxylene from $913/ton in February to $1,140/ton in early March. While Middle East instability has disrupted Paraxylene supply, LOTCHEM has stocks to last through April and is exploring alternate sources in Oman, Brunei, and China.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.