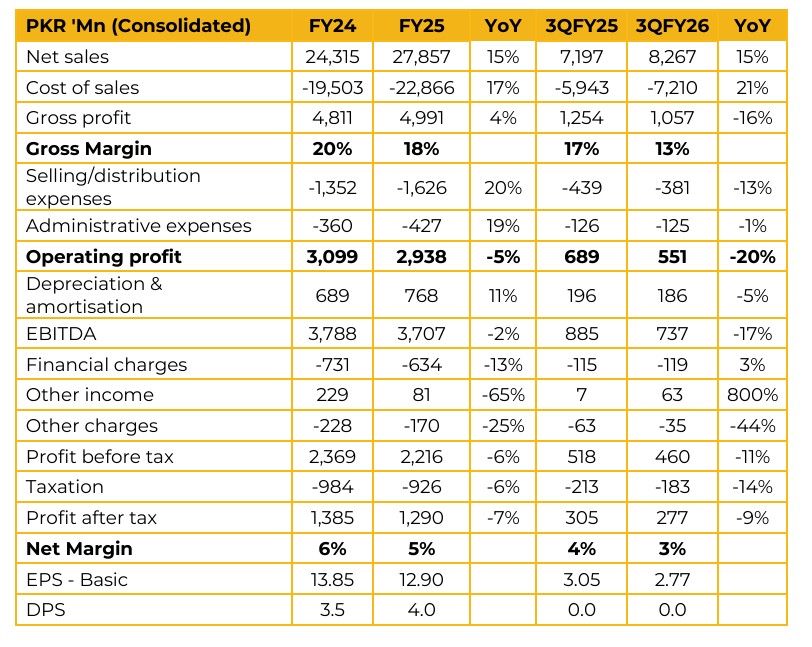

Ittehad Chemicals Limited (ICL) reported consolidated earnings per share of PKR 12.90 for FY25, compared to earnings per share of PKR 13.85 in FY24. Furthermore, in 3QFY26, the company reported earnings per share of PKR 2.77, compared to earnings per share of PKR 3.05 in the same period last year (SPLY). Management noted that recent quarters witnessed some pressure due to rising raw material and energy costs.

The increase in LABSA raw material costs was passed on in full to customers. Management also confirmed that depressed gross margins in the last quarter were partially due to SNGPL arrears, which it considers a one off item, while the matter remains under litigation.

The biomass power plant is designed to achieve complete energy self sufficiency by utilizing agricultural residues. The project cost is estimated at approximately PKR 10bn and will be financed through a 70:30 debt-to-equity structure. Commissioning of plant is expected in FY27. ICL is also installing a new flaker plant to enhance capacity by 16,500 metric tons per annum. The project is expected to be commissioned by September 2026 and is aimed at increasing the company’s share in both local and export markets. ICL has invested in fuel efficiency improvements for its gas fired power plant, resulting in a 9% improvement in efficiency.

The company exports to the Middle East, Central Asia, Europe and Australia, and has recently started exporting to the USA. The average power requirement for the chlor-alkali and caustic soda operations stands at around 30–32MW. Currently, the mix between gas and other energy sources is adjusted based on relative pricing. The reduction in super tax from 10% to 8% is expected to have a positive impact on the company.

However, there were no changes in the duty structure for caustic soda or LABSA. ICL Power was created as a separate subsidiary to take advantage of tax exemptions available for biomass energy projects. Exports currently represent around 5% of revenue. Management aims to increase this share to 7–10% following the completion of the flaker expansion.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.