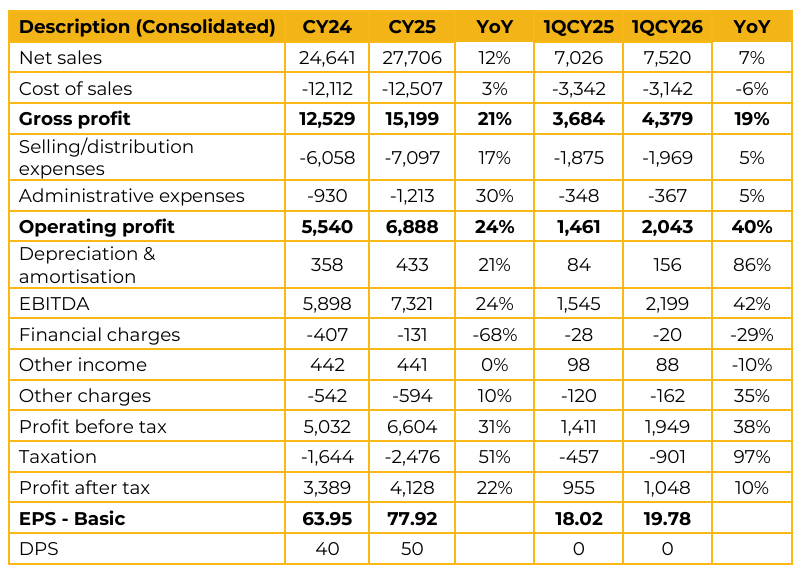

Highnoon Laboratories Limited (HINOON) reported consolidated earnings per share of PKR 77.92 for CY25, compared to earnings per share of PKR 63.95 in CY24.

Furthermore, in 1QCY26, the company reported earnings per share of PKR 19.78, compared to earnings per share of PKR 18.02 in the same period last year (SPLY). Highnoon Laboratories Limited is currently ranked 13th among more than 700 pharmaceutical companies in Pakistan and has delivered a 10 year CAGR of 22%, significantly outperforming the industry average growth of 15%.

The company is undertaking a capex program of PKR 6–7bn to establish a new state of the art manufacturing facility in a Special Economic Zone in Sheikhupura, with commercial operations expected to commence by mid 2029. Phase 1 of the expansion will focus on shifting existing product lines, particularly solid dosage forms, to the new facility.

While this phase will represent nearly 40% of total modules in volume terms, it is expected to contribute around 60% of revenue, primarily driven by the production with higher value products at the new facility. Phases 2 and 3 will focus on expanding the company’s product portfolio through the addition of new formulation lines and dosage forms not currently part of its existing portfolio.

Management specifically highlighted injectables, pre-filled syringes, and other therapeutic segments as key focus areas. The new facility will benefit from a 10 year tax exemption, with management expecting nearly 80% of the company’s revenue to eventually originate from this tax exempt plant. The company’s product portfolio currently comprises 40% essential drugs and 60% non essential drugs.

Management disclosed that the company is currently evaluating a potential acquisition. Financial due diligence has been completed, and an MoU is in the process of being signed, while specific details regarding the target remain undisclosed pending board and shareholder approvals. Highnoon Laboratories Limited maintains a strong market position in the respiratory and cardiology segments. Its flagship brand, Combivair, was the first Dry Powder Inhaler launched in Pakistan.

Management plans to launch 17 new products in 2026, including 11 in chronic care and six in primary care. These launches are expected to generate approximately PKR 1bn in annualized revenue over a 12 month period. Approximately 80% of the company’s cost base remains import dependent, with sourcing primarily from India and China.

Despite geopolitical disruptions, including the ongoing Iran United States conflict, management indicated that supply continuity remains intact through sea freight and airfreight alternatives where required. Suppliers had proposed price increases of 10–15% in response to elevated fuel and energy costs; however, the company leveraged its strong cash position to negotiate more favorable terms and, in certain cases, secure lower API prices.

The company currently maintains distributor inventory of approximately 75 days, which remains above the industry average. In the most recent quarter, revenue growth of 12% was driven by a 7% increase in volumetric sales and a 5% increase in pricing. Exports to Afghanistan, which account for nearly 6% of total revenue, remained under pressure due to border and regulatory disruptions, resulting in an estimated PKR 400mn revenue impact in 1Q.

Management highlighted that the majority of its product portfolio remains competitively priced. While Loprin has reached its MRP ceiling, other products still retain pricing headroom without requiring hardship appeals. Management expects two additional products to cross the PKR 1bn revenue mark by year end. Currently, nearly 40% of the company’s domestic contribution is derived from its top 10 products.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.