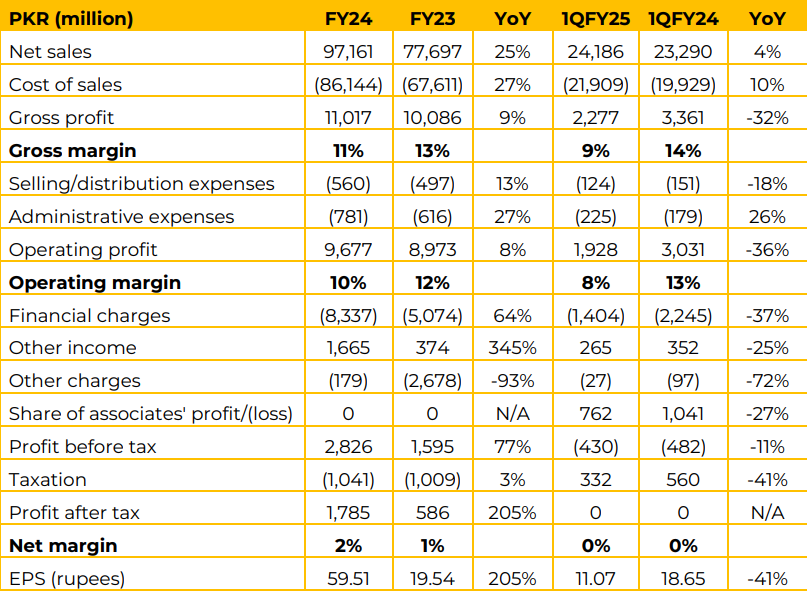

Fazal Cloth Mills Limited reported net sales of PKR 97.2 billion in FY24, a 25% increase YoY, driven by inflated prices. For 1QFY25, sales grew modestly by 4% YoY to PKR 24.2 billion.

The gross margin declined from 13% in FY23 to 11% in FY24, due to input cost pressures. For 1QFY25, the gross profit fell significantly by 32% YoY to PKR 2.3 billion, with margins compressing further to 9% from 14%. Financial charges surged by 64% YoY in FY24 to PKR 8.3 billion, driven by higher borrowing costs, though they declined by 37% YoY in 1QFY25.

The company will not under-take any BMR project until the policy rate is reduced to 10% or less. EPS surged by 205% YoY in FY24 to PKR 59.51.

However, in 1QFY25, EPS declined sharply by 41% YoY to PKR 11.07. The management highlighted that they are expanding solar capacity to the fullest. LCs are being opened for the addition of 5-6 MW solar plant (present 12 MW). The power plant is expected to be added in the ongoing fiscal year.

Moreover, the company also runs 51.3 MW of gas captive power plant. However, there is anticipation of gas supply cut, therefore the company has a backup of bagasse and coal power plant from Fatima Energy (associated company). Total power requirement of the company is 42 MWs.

Going forward, the management anticipates sales revenue growth in FY25, supported by recovery in Large Scale Manufacturing (LSM).

This growth is expected to be further bolstered by declining interest rates, stable exchange rates, and easing inflationary pressures, which collectively foster a favorable business climate. The company is also focused on cost optimization, including the addition of solar power capacity to mitigate rising energy costs.

Additionally, declining domestic cotton production underscores the need for research to develop higher-yield varieties. Despite these headwinds, the management remains optimistic about leveraging improved operational efficiencies, a supportive external environment, and export market recovery to deliver sustainable growth in FY25.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.