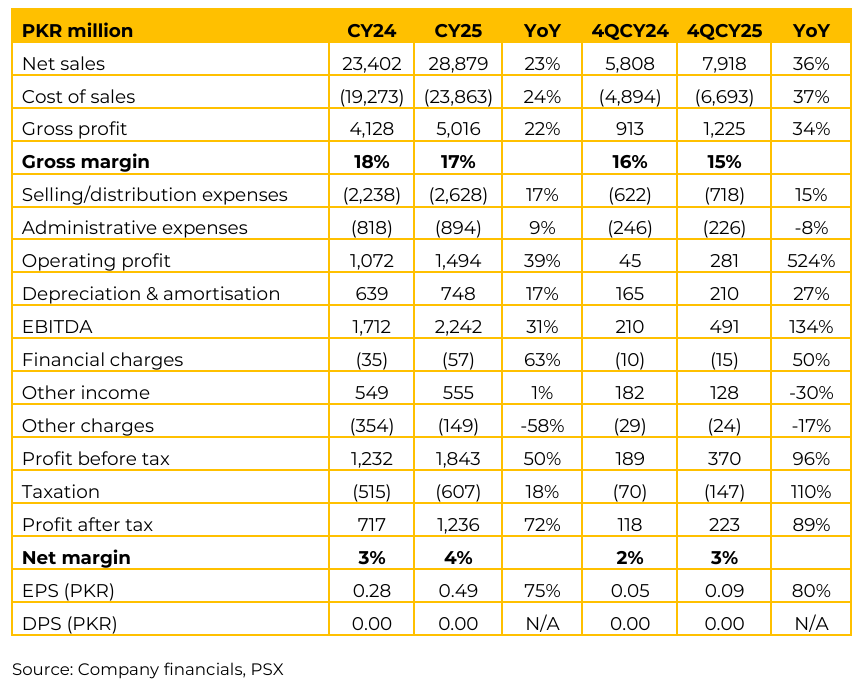

FFL has posted earnings per share of PKR 0.49 in CY25 (CY24: PKR 0.28). Moreover, in 4QFY25 the company marked an EPS of PKR 0.09 as compared to EPS of PKR 0.05 in 4QCY24. Management highlighted that company’s revenue grew from PKR 12 billion in 2022 to PKR 29 billion in 2025, representing a 32% CAGR.

Recent sales tax implementations have caused an industry-wide dip in sales volumes; however, FFL’s volume reduction has been significantly less than the industry average. The cereal business is now fully consolidated in FFL’s accounts. The pasta brand serves both B2B (industrial/restaurants) and consumer segments.

The acquisition of the pasta business in 2024-2025 has transitioned FFL into a multicategory powerhouse. While OPA pasta is currently under common management, it remains a separate legal entity from FFL. The company is aggressively pursuing high-margin segments through innovation and international trade. Buffalo milk powder is currently being exported to China. Skimmed milk powder is a key focus for the export pipeline.

While, research & development is underway to introduce camel milk powder as a high-margin export product. Going forward, management anticipates a 10% or higher increase in raw milk prices starting in the lean season (May–September), driven by rising fuel prices and potential environmental factors like floods. While the PKR is currently stable around 279-280, any significant rupee devaluation poses a risk to packaging material costs.

Despite generating healthy cash flows and profits, FFL intends to reinvest in the business to fuel further growth in the near term. Consequently, no dividend payout is currently planned, though final decisions rest with the Board.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.