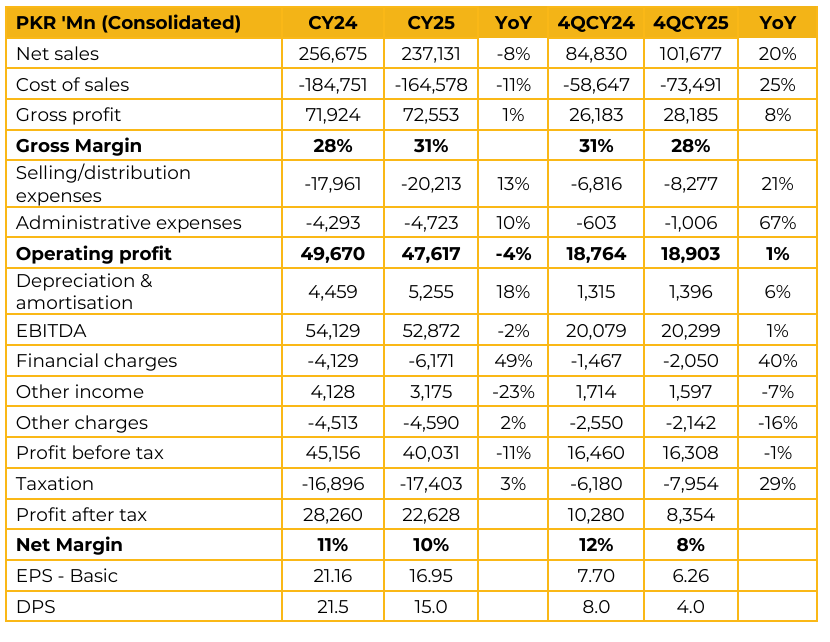

Engro Fertilizers Limited (EFERT) reported earnings per share of PKR 16.95 for CY25, compared to earnings per share of PKR 21.16 in CY24. Furthermore, in 4QCY25, the company reported earnings per share of PKR 6.26, compared to earnings per share of PKR 7.70 in the same period last year (SPLY).

Farmers faced pressure early in the year as wheat prices declined to PKR 1,800/maund; however, the government’s support price of PKR 3,500/maund later in the year significantly improved farmer liquidity and purchasing power.

Company inventory levels improved to 23% compared to 28% last year, with management noting that industry wide inventory levels are now at reasonable levels after remaining elevated in previous quarters.

The 20% decline in profit was attributed to three major factors, each impacting earnings by approximately PKR 2bn: Super Tax, higher finance costs due to carrying elevated inventory levels throughout the year, and increased freight charges associated with managing and distributing that inventory.

The company declared an 89% payout, slightly lower than prior levels. This reflects a prudent, liquidity driven decision by the board to retain cash in anticipation of potential adverse legal or regulatory outcomes related to GIDC. Management clarified that there is no change in the long term dividend policy.

The Pressure Enhancement Facility represents a total industry wide commitment of approximately USD 300mn. Phase 1 (piping infrastructure) has been completed, while Phase 2 (compressors) has experienced slight delays, with completion now expected by late Q3 or early Q4 CY26.

EFERT’s urea is more expensive than competitors due to higher gas costs; however, the company is currently offering a PKR 150 discount to align with industry pricing while evaluating a potential full withdrawal of the discount.

Urea demand appears robust, supported by improved farm economics and better water availability.

Management noted that despite energy price increases, the combined cost of urea and diesel constitutes less than 10% of a farmer’s total input cost. As long as wheat support prices remain above PKR 3,500/maund, urea demand is expected to remain strong, historically not falling below 6.3–6.4mn tons.

Management explicitly clarified that the company is not currently extending loans to Engro Corp or EPCL. The approval obtained represents a reciprocal arrangement aimed at providing financial flexibility at the group level, if required.

The company’s contract with SNGPL is set to expire in March 2027.

Management noted that the industry remains import dependent for DAP and is actively engaging with the government to ensure adequate imports and availability ahead of the peak application season later in the year

A key driver of the elevated debt levels is the industry wide PEF project, which requires approximately USD 100mn of financing on company’s end.

DAP is currently imported from Saudi Arabia, Morocco, and China.

The indigenous gas utilized is of low BTU, making it well suited for fertilizer production but less viable for other industries. As a result, management believes there is minimal risk of diversion of this gas to other sectors.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.