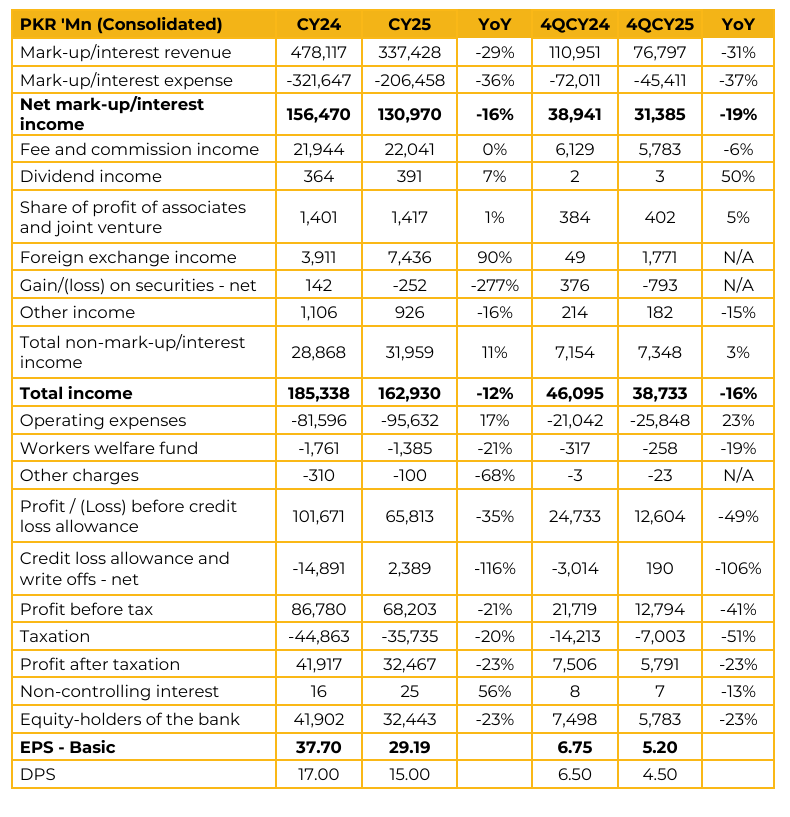

Bank al Habib Limited (BAHL) reported Consolidated earnings per share of PKR 29.19 for CY25, compared to PKR 37.70 in CY24. Furthermore, in 4QCY25, the company reported earnings per share of PKR 5.20, compared to earnings per share of PKR 6.75 in the same period last year (SPLY).

Total assets grew to PKR 3.3 trillion. Total deposits reached PKR 2.6 trillion, while investments stood at PKR 2.0 trillion.

The Non-Performing Loan ratio stands at 4.26%, which management described as stable despite pressures in the steel and textile sectors. Major NPL exposures have been either collateralized or restructured.

Current accounts constitute 36% of total deposits. When combined with savings, the overall CASA mix stands at approximately 89%

Management is targeting a deposit growth rate of 16% to 17% for CY26.

Approximately 85% of the investment book consists of floating rate instruments, primarily comprising floating PIBs and Sukuks. Fixed rate exposure remains limited, with fixed PIBs accounting for only 10% of the portfolio, with average yields of around 12% to 13%.

Following a rapid expansion in 2025 (112 new branches), the bank is now shifting toward consolidation. For 2026, it plans to open only 33 new branches. Islamic banking now accounts for 30% of the total branch network (392 branches as of year-end). The bank is actively converting conventional branches into Islamic ones.

The cost to income ratio remains elevated at around 60% due to recent aggressive branch expansion and remittance marketing costs. Management expects this to improve as expansion slows and consolidation takes effect. BAHL maintains a 12% market share in foreign trade, handling USD 6.1 billion in imports and USD 4.9 billion in exports. The bank processed USD 2.9 billion in remittances during CY25.

Management commented that recent treasury auctions reflect market expectations regarding interest rates. They expect net interest margins to improve as investments reprice and deposits grow.

Regarding the new SBP market risk guidelines, management indicated there may be some impact on the surplus, however, the current CAR of 17.01% provides a comfortable buffer.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.