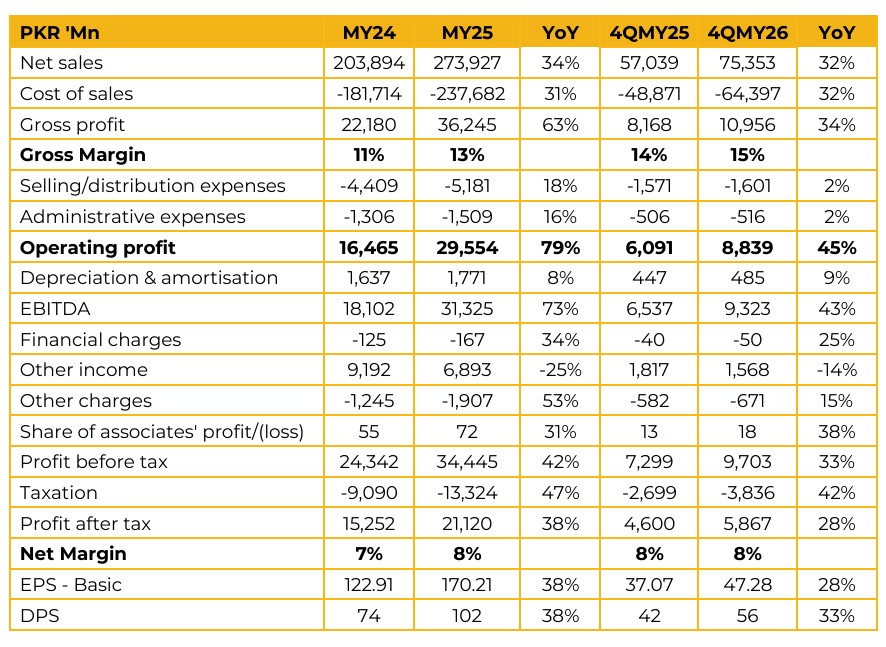

Atlas Honda Limited (ATLH) reported earnings per share of PKR 170.21 for MY25, compared to earnings per share of PKR 122.91 in MY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 47.28, compared to earnings per share of PKR 37.07 in the same period last year (SPLY). The automotive industry recorded production of 1.9mn units, with the motorcycle and three wheeler segment posting 32% growth.

The company achieved an all time high gross profit margin of 13.2%, supported by continuous cost reduction initiatives and an improved sales mix. The company also installed 9.8MW of solar power capacity. In 2017–18, the market had more than 100 Chinese players with nearly 50% market share. However, due to currency devaluation and limited localization, nearly 90% of them were unable to sustain their cost structures. Today, only 10–12 players remain, with their combined volumes declining from 1.4mn units to roughly 400k units.

The company’s rated capacity stands at 1.65mn units, but demand has now exceeded this level. Atlas Honda is investing PKR 5–6bn in capex to expand engine plant capacity, which remains the key bottleneck. The new capacity is expected to come online by Dec 2026. If demand in the ICE segment continues to grow, management intends to further increase engine plant capacity by 200k units.

Around 90% of new entrants are operating in the LAB segment, which uses lead-acid batteries with a battery life of only 12–18 months. Quality EVs use lithium batteries, which last around five years but cost over USD 1,000, making them less competitive without higher subsidies. Atlas Honda is closely monitoring the LAB segment but continues to prioritize global safety standards. Value-added bikes, mainly 100cc and above, now account for nearly 40–45% of the market, while the 70cc segment accounts for the remainder.

Atlas Honda leverages its position as the country’s largest buyer to strengthen its negotiation power and maintains a 3–6-month inventory buffer to stabilize margins. If inflation and the exchange rate remain stable, management expects double digit growth. The industry could return to its peak volume of 2.7mn units within the next three years. Rural demand accounts for 50–65% of the total market, and improved crop prices are expected to have a very positive impact on consumer cash flows and support double digit growth prospects.

The Icon E is currently based on a 100% imported CKD kit and uses high quality lithium technology rather than cheaper lead acid cells. Localization of the Icon E is expected to begin this year and may take 2–3 years to reach ICE level localization. Spare parts sales grew by 38% last year. The company’s strategy is to continue competing with the informal and smuggled parts market through vendor quality and scale, while targeting double digit growth over the foreseeable future.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.