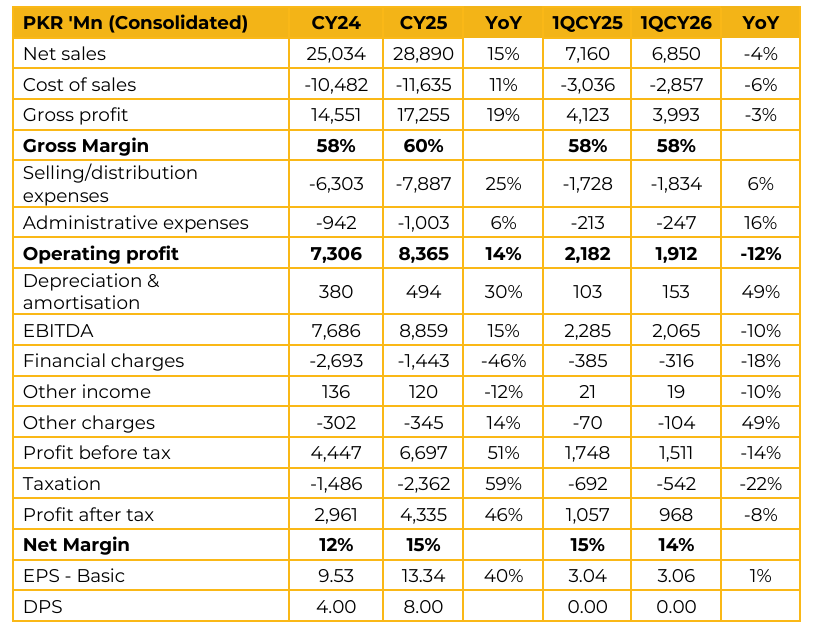

AGP Limited (AGP) reported consolidated earnings per share of PKR 13.34 for CY25, compared to earnings per share of PKR 9.53 in FY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 3.06, compared to earnings per share of PKR 3.04 in the same period last year (SPLY).

The most significant development during the period was the proposed merger of OBS AGP, which manages the Sandoz portfolio, OBS Pakistan, which manages the Pfizer portfolio, and OBS Pharma, which manages the Bayer portfolio, into AGP Limited. Following the merger, minority shareholders in the subsidiaries will receive AGP shares, resulting in a fully consolidated corporate structure with no non-controlling interest remaining. New shares under the scheme are being issued at a multiple of 10.4x. Following board approval, the merger process has entered the legal stage.

Management expects the court to direct an EOGM by the end of June 2026, while final court approval for the scheme is anticipated within the next four to five months. The merger scheme is effective from January 1, 2026, implying that AGP’s full year 2026 financial statements will reflect the performance of the combined entity. On a pro forma basis, 2025 revenue would have increased to PKR 37.5 billion, while profit would have stood at PKR 5.6 billion.

Management expects the consolidated long term debt of PKR 15.9 billion to be fully repaid by CY30. OBS Pharma adds a dominant women’s healthcare franchise to AGP’s portfolio, with gross margins of approximately 52% and several leading research based brands. AGP recently secured commercialization rights for Viagra and Xanax in Pakistan. Management expects both products to evolve into billion rupee brands over time, supported by strong brand equity and a large addressable market driven by the country’s sizeable diabetic and Erectile Dysfunction patient population.

While the currently documented Viagra market is estimated at PKR 400–500 million, management believes the long term market opportunity is substantially larger. AGP entered into a collaboration with STADA in 2026, securing marketing and distribution rights. Management highlighted that the first consumer healthcare and skincare products under the partnership are expected to be launched this month.

AGP is also working with the Bill & Melinda Gates Foundation on multi micronutrient supplements focused on maternal health. Management believes this initiative could provide a first mover advantage and create potential export opportunities through global procurement programs.

OBS Pharma is expected to contribute approximately PKR 9 bn in annual revenue and PKR 1.4 bn in profit. Management highlighted that gross margins at OBS Pharma have improved to approximately 52% over the last 1.5 years through operational enhancements. Going forward, management has set an ambitious target of increasing gross margins to 60% by the end of CY26. The OBS Pharma portfolio comprises approximately 77% non essential products and 23% essential products. In terms of sourcing, around 60% of raw materials are imported, while the remaining 40% are procured locally. AGP is currently commercializing products across 31 new markets, primarily in Africa and South America.

While management expects it to take 12–15 months before these markets contribute meaningfully, they believe the long-term revenue potential could match or exceed current sales generated from Afghanistan. Management identified the reopening of the Afghanistan border as the most significant near term catalyst, with expectations that the issue could be resolved within the next two to three months.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.