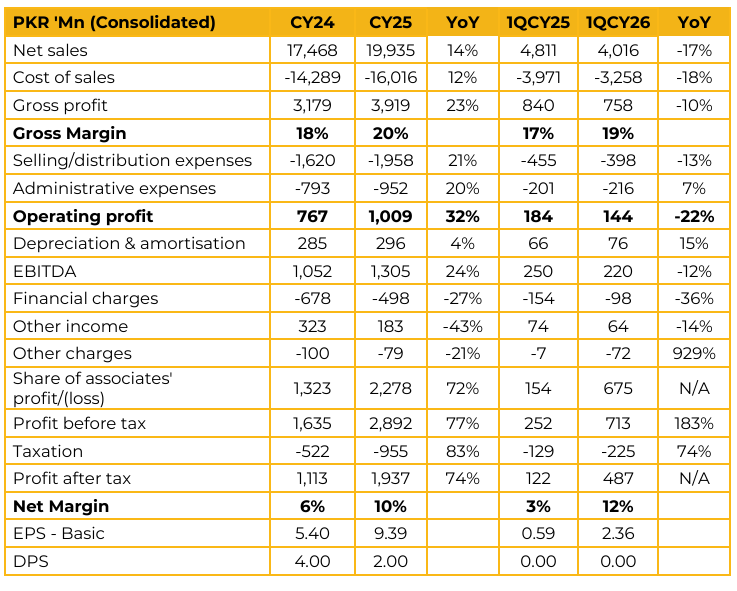

Service Global Footwear Limited (SGF) reported earnings per share of PKR 9.39 for CY25, compared to earnings per share of PKR 5.40 in FY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 2.36, compared to earnings per share of PKR 0.59 in the same period last year (SPLY). SGF operates a production facility in Muridke with an annual production capacity of 4.6 mn pairs.

SGF has incorporated Service Athletic Global Footwear, a joint venture with a Chinese partner. While SGF’s existing operations primarily focus on leather footwear, SAGF will target synthetic and athletic footwear production. Management indicated that trial production at SAGF is expected to commence in approximately six to eight weeks. Initial production will focus on local batches before transitioning toward export orders. The facility is expected to have an annual production capacity of 2 million pairs, followed by a phased capacity expansion to 5 million pairs and ultimately 10 million pairs in subsequent stages. Management highlighted that synthetic and athletic footwear generally carry lower average selling prices and tighter gross margins due to intense global competition.

However, the SAGF model offers stronger volume potential and operational efficiencies due to larger SKU sizes, allowing higher production volumes. The company recently invested approximately PKR 1.5 billion, primarily toward the development of the SAGF facility and broader growth initiatives during 2025. Management noted that no major capex is currently required. Management clarified that the reported liability stems from the share of profit attributable to SLM. Under accounting standards, SGFL is required to recognize deferred tax liabilities against undistributed reserves and profits. Long term borrowings increased to PKR 1.2 billion to support the construction of SAGF facilities and broader capacity expansion initiatives.

Meanwhile, short term borrowings were maintained at PKR 6 billion despite sales growth of 14%, supported by improved working capital management Leather accounts for approximately 45% of total product cost, with nearly 90% sourced locally, providing a natural hedge against currency volatility. For the new athletic footwear segment, specialized soles including EVA and rubber components will be imported from China and are expected to account for approximately 10% of total shoe cost. Gross margins recovered from 16% in 2024 to 18% in 1Q2026, supported by internal operational efficiencies. Management believes SGF maintains a competitive advantage over China and Vietnam in leather footwear production.

Management attributed the decline in first quarter volumes to the reversal of tariff related advantages previously enjoyed against China, resulting in certain brands shifting production back to China. In addition, global mid-tier brands experienced an overall sales decline of approximately 10%–15% due to Middle East tensions and inflationary pressures in Western markets. Management expects demand recovery during the second half of 2026. Management intends for SAGF to adopt a business model similar to SFL, with more than 90% of production expected to be export oriented. The new synthetic and athletic footwear facility will also operate under a contract manufacturing model. Management expects the 15% tax rate on dividends received from Service Long March to continue going forward.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.