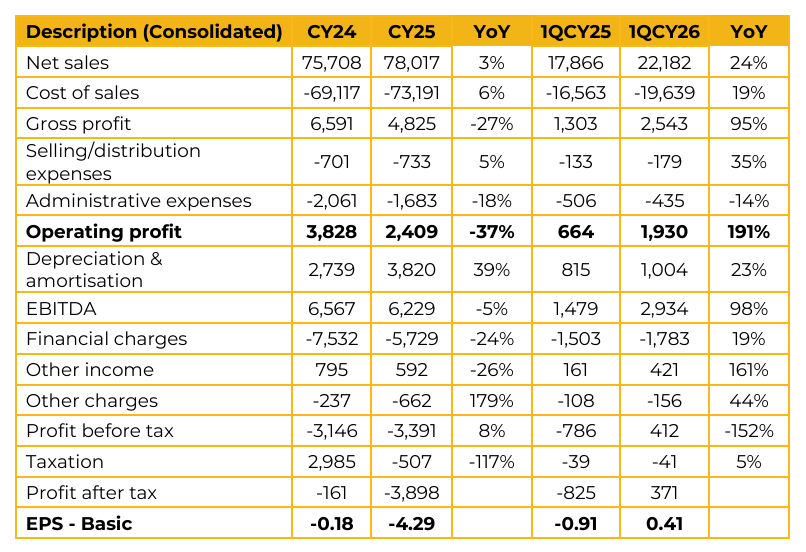

Engro Polymer Chemicals Limited (EPCL) reported consolidated loss per share of PKR 4.29 for CY25, compared to loss per share of PKR 0.18 in FY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 0.41, compared to loss per share of PKR 0.91 in the same period last year (SPLY). Domestic volumes grew by 26% in 2025. Prices rebounded during 1Q2026 following China’s removal of tax rebates on exports; however, management highlighted that prices have started to soften again during May 2026.

Caustic soda performance remains stable, although margins continue to face pressure due to the captive gas levy, as competitors operating on coal or grid power are not exposed to this additional cost burden. The new HPO plant became operational in February 2025 and achieved a market share of 32% by year end.

The company also secured anti dumping duties for a five year period against imports from seven countries to protect local industry margins. To mitigate elevated gas costs of approximately PKR 47 per unit, EPCL is aggressively pursuing a PKR 10 billion project aimed at converting its power supply from captive gas generation to the national grid. Regarding HPO, management highlighted that although the plant was originally designed by the licensor for a capacity of 28kta, the company has successfully tested and demonstrated an annualized production capacity of 31.5kta.

The company is also installing a 2MW solar project at its site, with the first batch of panels expected to become operational immediately. Lotte Chemical Pakistan Limited is currently conducting due diligence for the potential acquisition of Engro Holdings’ stake in EPCL. Management expects a decision by June 2026. The existing preference shares will remain in place regardless of the transaction until their respective call or put options are exercised or expire. In recent months, the company has continued to receive uninterrupted gas supply for operations. Although the plant recently underwent a three week maintenance shutdown, management confirmed that operations have since resumed successfully.

The company consumes approximately 20mmcfd of gas, of which nearly 75%–80% is utilized for power generation at a tariff of around PKR 3,500 plus an additional PKR 1,400 levy, while the remaining 20% used for process requirements, including furnaces and boilers, is charged at a lower tariff of approximately PKR 2,200 2,400. Under the current pricing framework, the levy stands at approximately PKR 1,400 per MMBtu.

However, management indicated that if the government adopts a weighted average peak/off-peak pricing mechanism, the levy could potentially decline to around PKR 550–600 per MMBtu. Currently, captive gas-based power generation costs approximately PKR 47 per unit, which declines to around PKR 36 per unit after incorporating steam turbine credits.

Management believes that transitioning to grid power could reduce power costs to approximately PKR 27–32 per unit, resulting in meaningful savings at the bottom line level. Management remains optimistic that PVC prices will remain within a sustainable range for the business, despite observing softer trends in international markets. Regarding PVC, management highlighted that EPCL currently has a review underway with the National Tariff Commission regarding dumped imports originating from the US and Indonesia.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.