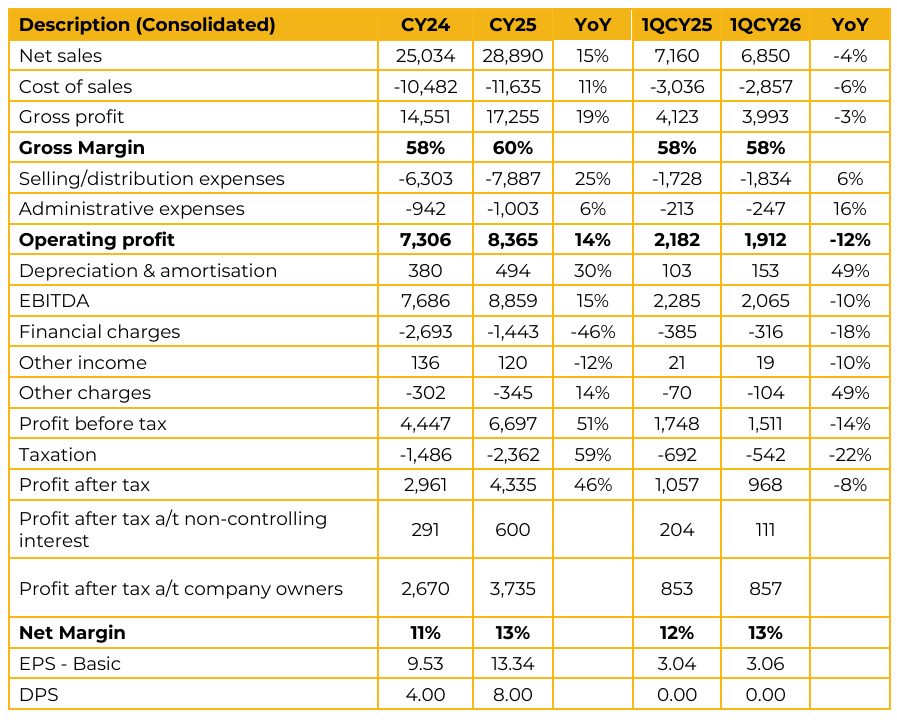

AGP Limited (AGP) reported consolidated earnings per share of PKR 13.34 for CY25, compared to earnings per share of PKR 9.53 in FY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 3.06, compared to earnings per share of PKR 3.04 in the same period last year (SPLY)

The company operates three manufacturing facilities in Karachi, comprising a general medicine facility, a dedicated cephalosporin plant, and a nutraceutical manufacturing facility. The portfolio’s leading blockbuster brand is Azomax, contributing approximately PKR 4.8bn in sales, followed by Rigix PKR 4.3bn, Osnate PKR 2.4bn, and Norvasc PKR 2.0bn. AGP has entered into a new strategic alliance with Stada, a German entity, for the Olatum consumer healthcare and skincare portfolio, which includes lotions, washes, and baby soaps. The company has secured marketing rights for Viagra and Xanax from OBS Group, with commercialization commencing this month.

AGP is currently establishing a biotech facility, which is expected to become operational by 4QCY26. The plant will manufacture Semaglutide and Tirzepatide, GLP-1 molecules similar to Ozempic and Mounjaro, along with a range of insulin products. Management disclosed that the total capex for the biotech facility is estimated at PKR 500–600mn, primarily due to the availability of existing land and basic infrastructure. Despite land border closures with Afghanistan, AGP exported approximately PKR 2.5bn worth of products to the country during 2025 through air transportation. In 2026, the company has already achieved sales of PKR 1.2bn to the market.

Management believes the border is likely to reopen eventually, citing the risk of an impending healthcare crisis in Afghanistan. The company is also diversifying geographically by expanding into 31 new international markets across Africa, South America, and Asia to reduce dependence on a single export region. For 2026, management is targeting growth of more than 15%, compared to the industry growth outlook of 12–13%.

Management highlighted that although overall industry volumes were impacted by a shorter winter season and elevated inflation, AGP’s performance remained resilient due to its strategy of prioritizing volumetric growth over massiveprice increases.

Currently, around 85% of APIs are imported, primarily from China. Management explained that local API manufacturing remains a high volume, low margin business, requiring consistent government policy support over a 10–15 year horizon to become commercially viable

The company’s 2025 sales mix comprised 85% trade sales, 6% institutional sales, 9% exports, and 1% toll supply. Institutional sales during 1Q2026 stood at approximately PKR 650mn, representing nearly 9.5% of total sales. Management noted that Afghanistan previously attempted to source medicines from Uzbekistan through land routes; however, the initiative was unsuccessful. On a consolidated basis, approximately 65–70% of AGP’s portfolio comprises non-essential products.

AGP also leverages the broader group’s procurement scale to negotiate better API pricing through bulk purchases. Management highlighted that the elimination of input sales tax remains a key discussion point with the government. Since pharmaceutical companies are unable to charge sales tax on their final products, the input tax effectively becomes a significant cost burden.

Management noted that the taxation framework for exports was recently shifted from a fixed 1% tax regime to the normal tax regime. The company is lobbying for the restoration of the 1% fixed tax structure to support export oriented growth.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.