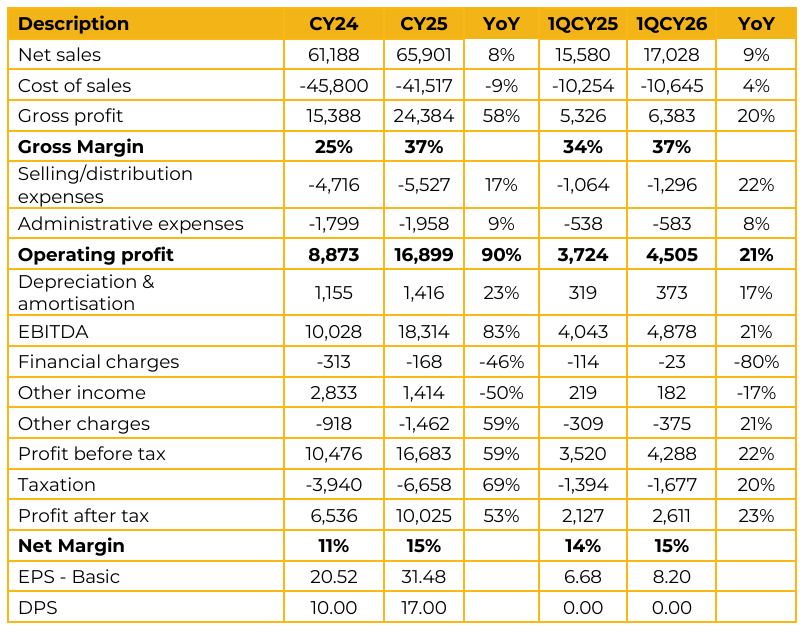

GlaxoSmithKline Pakistan Limited (GLAXO) reported earnings per share of PKR 31.48 for CY25, compared to earnings per share of PKR 20.52 in CY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 8.20, compared to earnings per share of PKR 6.68 in the same period last year (SPLY).

Glaxo is the leading pharmaceutical company in Pakistan by volume, with a 9% market share, and holds a 6% share in terms of value. Total sales reached PKR 66 bn, reflecting an 8% increase YoY. This growth was primarily driven by price adjustments, which offset a 10%–12% decline in sales volumes. Gross profit margins expanded significantly from 25% to 37%, representing a 12 percentage point increase.

This improvement was driven by responsible price adjustments and a series of profit sustainability measures. The product portfolio is led by VATES, contributing PKR 14 bn, followed by Augmentin at PKR 10 bn, while Velosef and Amoxil each contribute approximately PKR 5 billion, whereas Calpol accounts for PKR 4 bn. A key strategic milestone was the launch of Shingrix, a vaccine for adult immunization against shingles.

Management highlighted that adult vaccination represents a new category in Pakistan and is expected to gain traction gradually over time. The revenue mix comprises approximately 45% essential drugs and 55% non-essential drugs. Management attributed the decline in volumes to industry wide pressures, along with specific challenges in KPK and Balochistan. Security concerns and border closures have adversely impacted medical tourism, where patients from Afghanistan previously traveled to these regions for treatment.

These provinces contribute roughly 20% to GSK’s total sales. The company has withdrawn from low margin government tenders to protect profitability and has negotiated discounts with vendors through advanced payment mechanisms. Management has optimized the sales field force and reduced promotional allowances as local profitability improved.

While non essential drugs are now deregulated, essential medicines remain capped at approximately 7% of CPI. Management noted that they are awaiting government approval for 50–60 hardship pricing cases that have remained pending with the regulator for the past three years.

Approximately 80% of API costs are dollar linked. While current API prices remain stable, management cautioned that prolonged geopolitical tensions could impact API prices, whereas, as of now, freight prices have been increased only. Despite the growing shift toward local generics, management remains confident in the company’s brand equity, emphasizing that product quality and trust remain key decision drivers for healthcare providers.

The pharmaceutical sector faces a high effective tax rate , including a 1% Clinical Research Fund levy on gross profits. Management is advocating for rationalization of the tax regime and a more consistent, long term industrial policy to reduce regulatory uncertainty.

Government tenders account for approximately 7%–8% of total sales and are typically concentrated in the fourth quarter due to procurement cycles. GSK sources its APIs from a diversified base, including Europe, China, and India.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.