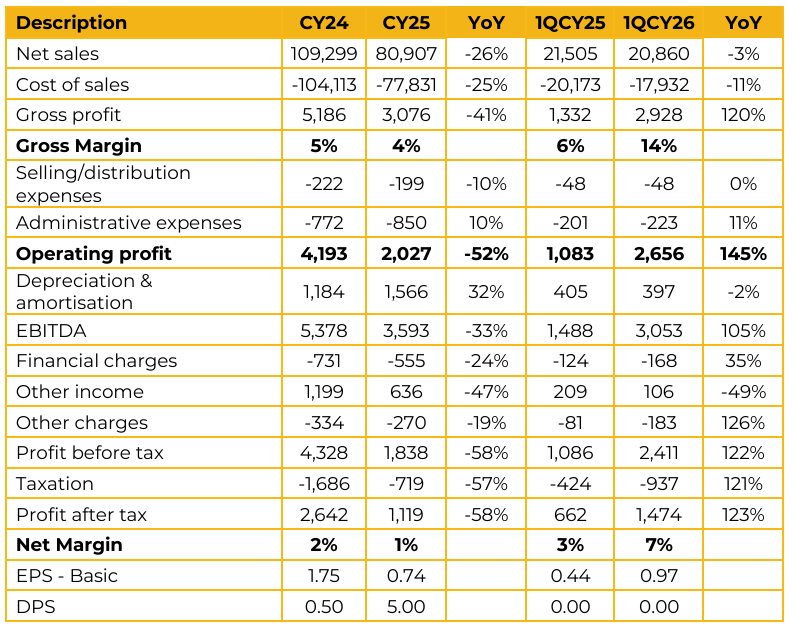

Lotte Chemical Pakistan Limited (LOTCHEM) reported earnings per share of PKR 0.74 for CY25, compared to earnings per share of PKR 1.75 in CY24.

Furthermore, in 1QCY26, the company reported earnings per share of PKR 0.97, compared to earnings per share of PKR 0.44 in the same period last year (SPLY). Lotte Chemical Pakistan Limited reported lower volumes and profitability during CY25 compared to the previous year.

Management attributed the decline primarily to weak domestic demand and increased competition from imports. Lotte Chemical Pakistan Limited remains the sole producer of PTA in Pakistan, benefiting from a natural dollarized hedge along with protective measures such as anti dumping duties on PTA imports.

Regarding the proposed acquisition of EPCL, management highlighted that due diligence is at an advanced stage, while commercial discussions with the seller are progressing toward the finalization of the SPA. Management noted that an existing wire connectivity between EPCL and Lotte is already in place, which represents a key strategic advantage for the proposed transaction.

Energy synergies remain the primary driver of the deal. EPCL currently operates on a captive gas based model, with an effective power cost of PKR 49–50 per unit. In comparison, Lotte is fully connected to the grid through 220KV transmission lines at an effective rate of approximately PKR 29 per unit. Management believes connecting EPCL to LOTCHEM’s grid infrastructure could generate annual savings of around PKR 10 bn.

Management expects to connect 55–60% of EPCL power load within the next couple of months under Phase I of the integration plan. Achieving full connectivity is expected to take 12–18 months and would require additional capex, mainly for transformer installation. The company’s BESS is now operational, eliminating the need for standby diesel generators and reducing conversion costs by approximately USD 5 per ton. Lotte Paraxylene supplier in Kuwait declared force majeure over two months ago. Management has since secured alternate feedstock supply from Oman. However, these are spot market purchases, and the higher procurement cost is being passed on to customers.

Management noted that its 220KV transmission line remains highly reliable, with minimal voltage or frequency disruptions compared to lower voltage grid connections. Sales to Novatex Limited declined significantly in 1QCY26. Management attributed this to a plant turnaround at Novatex and inventory build up of imported PTA ahead of the finalization of anti dumping duties in January. Sales have normalized in 2QCY26.

Management remains cautious on the demand outlook for the remainder of the year. The current demand remains intact, they anticipate broader demand destruction across the economy due to higher pricing. As a result, management expects overall volumes to remain under pressure while pricing stays firm. Total PTA demand in CY25 stood at approximately 750,000 tons, including volumes under the EFS for re-export purposes.

Domestic PTA demand remains lower than the headline figure. Regarding EPCL PKR 32 billion net debt, management stated that the focus remains on unlocking internal synergies, primarily energy savings, to generate sufficient cash flows for debt servicing and deleveraging.

Management indicated that selling electricity back to the grid is not currently a strategic focus, as they believe the long term economics of industrial cogeneration remain unattractive. Management also highlighted that there is currently limited visibility beyond June regarding raw material availability and pricing, as uncertainty across the global value chain continues to persist. Lotte power requirement stands at 26MW, while EPCL power requirement is approximately 54MW.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.