From Fixed-Line Incumbent to Integrated Digital Infrastructure Champion

PTCL management expects amalgamation approval (Ufone Telenor) by June 2026, with the first day of combined Ufone Telenor operations targeted for 3Q 2026. The transaction is expected to transform PTCL into the largest integrated telecom platform in Pakistan, with management aiming to become the largest and best telecom operator in the country. The combined customer base currently stands at around 73 million subscribers, and management expects this to increase to approximately 75 million customers by the time amalgamation is completed. Importantly, PTCL will also have the largest spectrum holding in Pakistan, which will position the company to offer the highest network speeds once infrastructure rollout and spectrum deployment are completed. Deployment at scale is already underway according to management.

Merger Synergies: Multiple Cost Lines in Play

Management highlighted several areas where material efficiencies are expected post-amalgamation. One of the most visible opportunities is network rationalization. Management stated that the monthly operating cost of one tower is around PKR 250,000–300,000, while the CCP report refers to the expected dismantling of around 7,000 overlapping sites. This alone points to a potentially significant cost-saving opportunity. Beyond towers, management also expects savings across:

Marketing: One unified brand should reduce duplication.

Sales and distribution: One channel structure should replace overlapping networks.

Administration and facility management: Consolidation should lower overheads.

Capex avoidance: A combined network footprint should reduce the need for duplicate investment. Management expects these efficiencies to become visible from 1Q 2027 and onwards.

ARPU Upside: Consolidation Creates Room for Monetization Management indicated that the current combined ARPU is around PKR 310, and expects this to rise going forward.

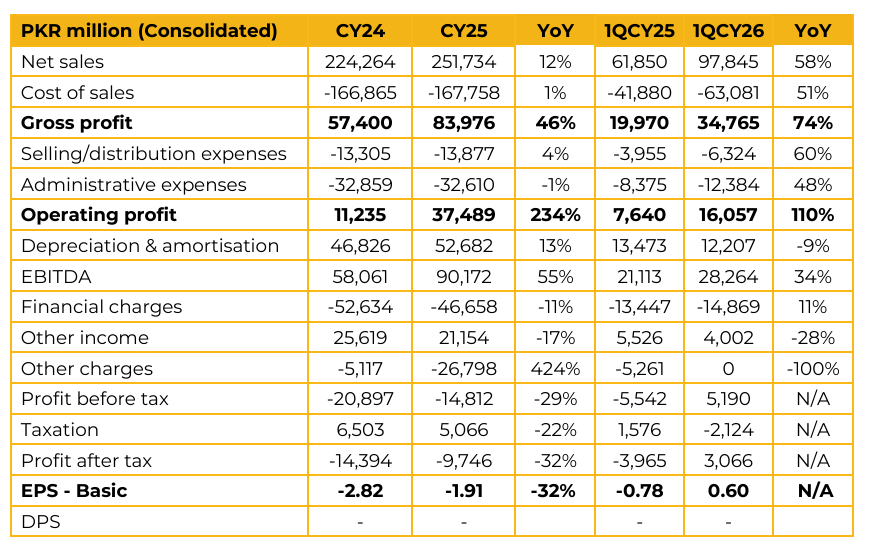

1Q Performance Already Reflects the Scale Shift

PTCL’s 1Q revenue and EBITDA grew by 58% YoY and 132% YoY, respectively, largely driven by the acquisition of Telenor Pakistan. This marks the first visible step-change in the size and operating leverage of the business.

Broadband: A Large Underpenetrated Growth Engine

Management remains highly optimistic on the broadband opportunity. PTCL currently has around 833,000 FTTH subscribers, and expects total connections to increase by 2–3x over the next four years by 2030. Management mentioned that Pakistan remains significantly underpenetrated, with broadband penetration at only 7.5% versus a peer average of around 29%. This gives PTCL a long runway to scale its fixed broadband business, especially as demand for high speed home internet continues to grow.

Cloud and Data Centres: Building the Digital Infrastructure Layer

PTCL also plans to double its cloud and data centre capacity by 2030. Current capacity stands at around 11MW. Management highlighted that PTCL’s cloud and data centre business has grown strongly over the last five years, with revenue and EBITDA CAGRs of approximately 34% and 27%, respectively. This business can become a key long-term growth pillar as enterprise digitization, cloud adoption, and data localization needs increase in Pakistan.

Fintech Optionality Through U Bank

Management also sees meaningful opportunity in fintech through U Bank. Pakistan remains structurally underbanked, with around 70% of the adult population unbanked, compared to a peer average of roughly 30%. Management also noted that only around 25% of telecom users currently have banking access. This creates a natural opportunity for PTCL to leverage its enlarged telecom customer base, distribution network, and digital infrastructure to participate in financial inclusion.

Tax Recoverable: Gradual Balance Sheet Release

Management also commented on the PKR 79 billion income tax recoverable, stating that this amount is expected to be adjusted gradually going forward. While timing may be phased, this remains an important balance sheet item to monitor.

Investment Takeaway

PTCL is entering a structurally different phase. The company is no longer just a legacy fixed-line operator with a small mobile operation; it is becoming a scaled telecom, broadband, cloud, data centre, and fintech platform.

The key drivers from here are clear: amalgamation approval, network integration, tower rationalization, ARPU uplift, broadband scale-up, cloud/data centre growth, and fintech optionality. If execution is delivered, PTCL’s earnings profile could shift meaningfully over the next few years, with the company positioned as the dominant integrated digital infrastructure player in Pakistan.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.