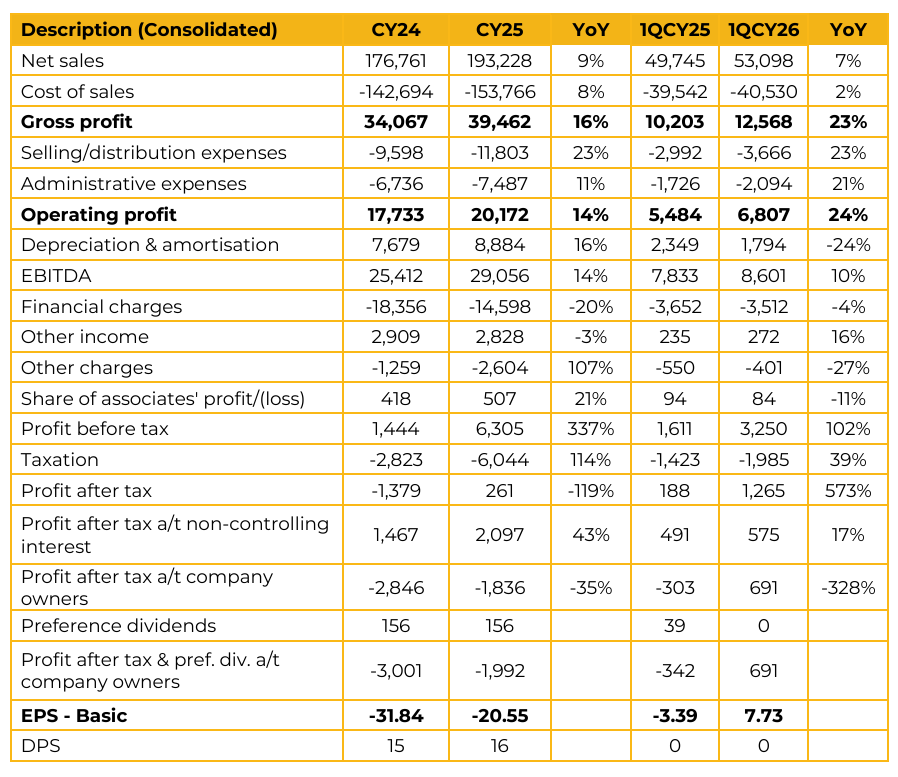

Packages Limited (PKGS) reported consolidated loss per share of PKR 20.55 for CY25, compared to loss per share of PKR 31.84 in CY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 7.73, compared to loss per share of PKR 3.39 in the same period last year (SPLY). In the packaging converter segment, turnover increased by 4% YoY to PKR 51bn. This segment comprises consumer products tissue, flexible packaging, and folding cartons. Bulleh Shah Packaging, a wholly owned subsidiary of the company, continues to show improvement, with management successfully reducing losses by 65–70% in 1Q2026 compared to SPLY.

Tri-Pack Films Limited witnessed a sharp recovery after a stagnant FY2025, reporting a 400% YoY increase in profitability in 1Q2026, with earnings reaching PKR 300mn. In the starchPack segment, the company successfully returned to profitability in 1Q2026, posting earnings of PKR 36mn after incurring significant losses in the previous year. On the persistent losses at Bulleh Shah Packaging, management explained that the company undertook a major PKR 28bn investment program starting in 2021 to expand capacity and improve operational efficiency.

However, the project faced significant challenges, primarily due to the sharp increase in interest rates, which coincided with the commissioning of new capacities and made it difficult to recover investment costs. Management also highlighted that the market has been facing significant dumping of imported paper, which continues to suppress local margins. Anti-dumping duties of up to 29% were implemented in December 2025; however, traders subsequently obtained a court stay.

As a result, while market prices have increased by 8–9%, the full impact of these duties has yet to be reflected. Management noted that customers are currently more focused on material availability amid supply chain disruptions rather than pricing. Around 90–95% of the power mix is based on local biomass. The shipping carton business, which accounts for 45% of the total product mix, relies on local waste paper and agricultural waste, providing relative stability. The primary risk remains wood pulp imports.

Management expects Bulleh Shah Packaging losses to narrow to 20–30% of the losses recorded in 2025. Management noted that freight costs and war-risk premiums have increased overall costs. However, given that packaging constitutes only 5–6% of an FMCG company’s total cost structure, customers have shown a willingness to absorb price increases to keep their production lines running.

Management clarified that while anti-dumping duties are specifically targeted at bleached board, the company’s core growth strategy remains focused on maximizing utilization at its Karachi corrugated plant to capture value across the full chain from paperboard to finished cartons.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose