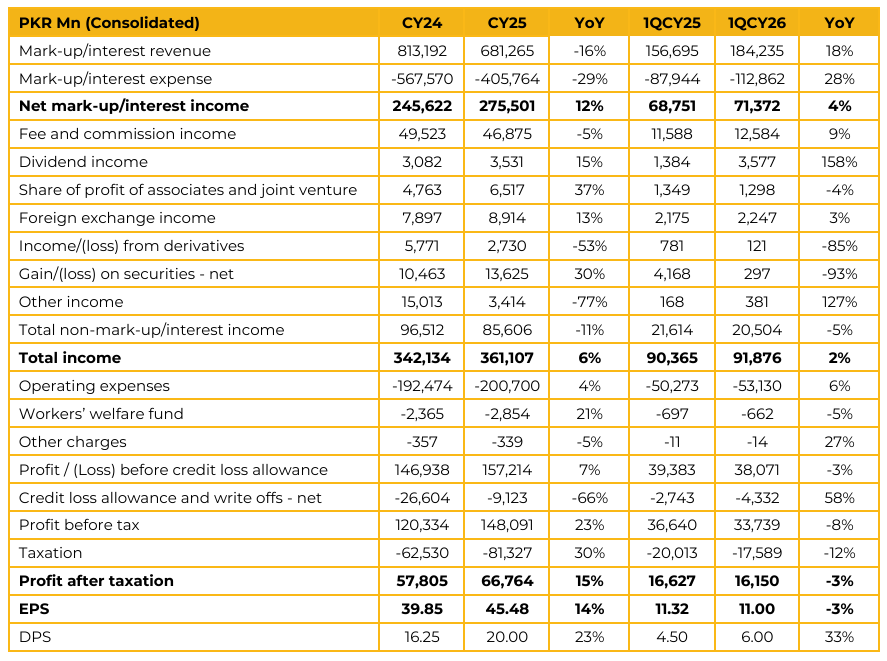

Habib Bank Limited reported consolidated earnings per share of PKR 11.00 in 1QCY26, down 3% from PKR 11.32 in 1QCY26. This translates into profit after tax of PKR 16.2 Bn compared to PKR 16.6 Bn in SPLY. The bank declared a dividend of PKR 6 per share in 1QCY26, up 33% from PKR 4.5 in 1QCY25.

Total revenue in 1QCY26 reached PKR 91.9 Bn against PKR 90.4 Bn in 1QCY25, an increase of 2%. This was primarily driven by a 4% increase in mark-up income from PKR 68.8 Bn in 1QCY25 to PKR 71.4 Bn in 1QCY26. The bank saw its total deposits drop from PKR 5.55 Trn at the end of CY25 to PKR 5.39 Trn at the end of 1QCY26, a decrease of 3%. Current accounts remained at PKR 1.77 Trn during the period and now form 38.6% of domestic deposits.

The management apprised that moving forward, they are targeting to maintain market share in deposits and placing a special emphasis on low-cost deposits. Investments stood at PKR 4.8 Trn at the end of 1QCY26, up 15% from PKR 4.2 Trn at the end of CY25. Management highlighted that out of its portfolio of investments of PKR 4.8 Trn, PKR 1,149 Bn is invested in fixed rate PIBs and PKR 2.5 Bn in PIB Floaters.

The portfolio also includes PKR 827 Bn in T-Bills. Average duration of the portfolio is about 1 year. The bank’s cost to income ratio for 1QCY26 stood at 58% compared to 56% in 1QCY25. Management aims to bring this down to below 50% in the medium term. Capital Adequacy Ratio stood at 16.7% at end Mar-26, down from 18.3% at the end of CY25. Moving forward, the management believes that the MPC has made the prudent decision by hiking the policy rate by 100 bps. According to management, this is sufficient to hold the line until the next MPC, while a smaller hike could have mandated an emergent meeting if the situation deteriorated further. Moving forward policy rate movement is heavily dependent on the war and global commodity prices. Management is confident of preserving profitability in this environment.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.