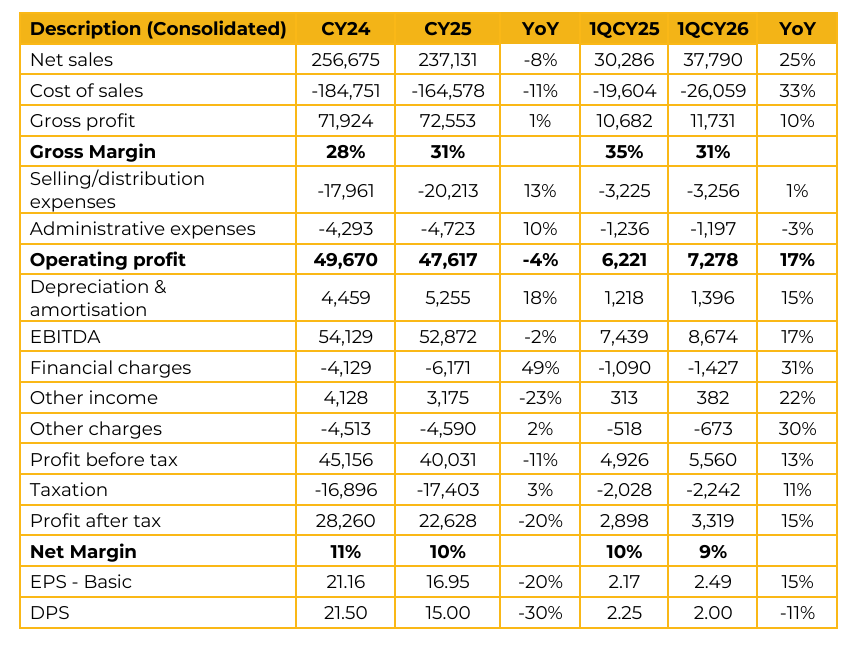

Engro Fertilizers Limited (EFERT) reported earnings per share of PKR 16.95 for CY25, compared to earnings per share of PKR 21.16 in CY24. Furthermore, in 1QCY26, the company reported earnings per share of PKR 2.49, compared to earnings per share of PKR 2.17 in the same period last year (SPLY). The current DTP price of urea stands at PKR 4,535 per bag, while the MRP is at PKR 4,749 per bag.

Dealer margins are currently around PKR 225 per bag. Urea prices have increased by PKR 100 per bag as of April. The company’s dividend policy remains unchanged. At the base plant, around 40% of gas is being supplied at a concessional rate of PKR 580/mmbtu. The company had assurance of this pricing as long as gas availability in the reservoir is sustained; previously, this allocation was provided on an availability basis. Urea sales for the company are expected to be in the range of 6.0 6.5 million tons for the year.

The Enven plant is priced at SNGP pricing. Packaging costs have also seen a sharp increase, with bag prices rising by approximately 100%. Borrowings have increased due to higher working capital requirements, while long term debt has risen to support ongoing capital expenditure projects.

The company currently holds DAP inventory. Given that DAP imports are routed through the Strait of Hormuz, management is exploring alternative supply routes to mitigate risk. Management highlighted that farmer economics have improved significantly compared to last year, with wheat prices rising by around 40% YoY, from PKR 2,300 to PKR 3,200 per maund. Unlike the drought conditions seen in the SPLY, the country is currently experiencing ample water availability, with levels at a multi-year high of approximately seven years. On production shortfalls, management noted that while some industry plants are currently offline or operating at reduced capacity, the government considers urea a critical commodity and is expected to restore gas supplies on a priority basis.

The 31% YoY increase in finance costs is primarily attributed to funding the PEF project, which remains the key capex item on the balance sheet for the year. Despite global supply chain disruptions stemming from the Middle East crisis, management confirmed that the PEF project has not been impacted and remains on track for completion in Q3.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.