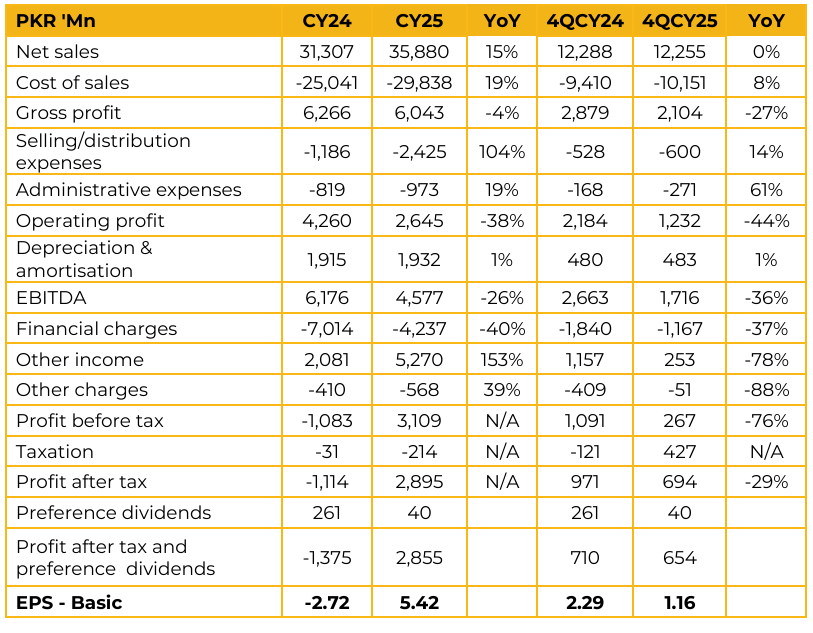

Agritech Limited (AGL) reported earnings per share of PKR 5.42 for CY25, compared to loss per share of PKR 2.72 in CY24. Furthermore, in 4QCY25, the company reported earnings per share of PKR 1.16, compared to earnings per share of PKR 2.29 in the same period last year (SPLY).

AGL achieved a 20% increase in sales volumes (390kt vs 325kt). The company’s market share in urea expanded from 5% to 6%, with dealer margins maintained at PKR 225 per bag. AGL utilizes locally sourced phosphate rock instead of imports, having adapted its technology following the Hazara Phosphate acquisition. The company maintains inventory coverage of approximately 4–5 months.

Currently, the company continues to operate under its previous arrangement on the Sui network at a gas price of PKR 1,597/MMBTU. The transition to Mari gas is ongoing and requires regulatory approvals, including an OGRA shipping license and Gas Transport Agreements with SNGPL. Upon completion, gas pricing will shift to Petroleum Policy rates.

The plant experienced a temporary shutdown of approximately two weeks at the onset of the Middle East conflict but is now fully operational. The company is currently benefiting from incremental gas flows from northern sources, driven by limited transmission capacity to other regions, thereby ensuring continued plant operations even when other sectors face curtailment. Despite elevated international urea prices, there are no indications of urea exports, as local production continues to be prioritized to meet domestic demand. While the company returned to a net profit of PKR 2.9bn, management highlighted that a significant portion of this positive bottom line was driven by one-off income and gains.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.