Key Takeaways:

• Introduction of fortified and premium products to cater to the health-conscious urban demographic.

• Positioning itself as a leader in branded staples, leveraging its Sunridge brand for premium pricing and consumer trust

• Plans for potential entry into landlocked markets like Azerbaijan and Uzbekistan for processed edible oil.

• Management aims to revert to FY23 revenue levels (PKR 100 billion) with a higher share of branded and value-added sales.

• Impact of declining interest rates to materialize from January 2025 onwards.

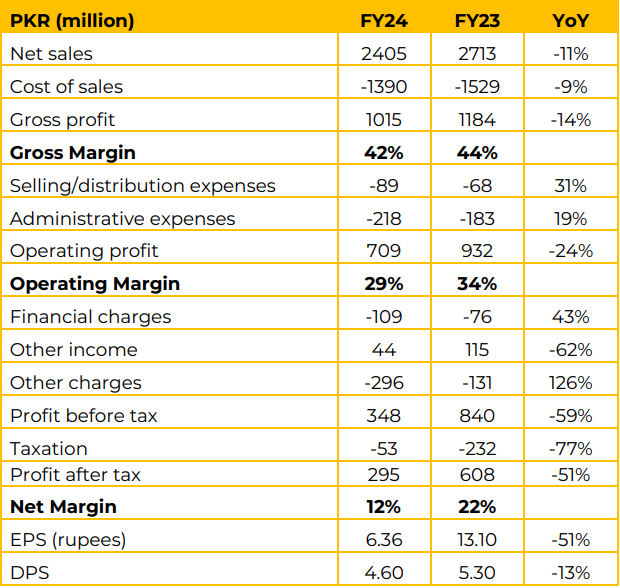

Unity Foods Limited reported a significant decline in net sales, with FY24 sales dropping by 18% YoY to PKR 83 billion compared to PKR 101 billion in FY23. The decline was steeper in 1QFY25, where net sales fell 22% YoY to PKR 18.4 billion. . The gross margin shrank to 9% from 14% in FY23.

However, in 1QFY25, gross profit saw a marginal YoY increase of 4% to PKR 2.7 billion, with gross margins improving to 14% from 11%. . Management highlighted a supply glut in the local edible oil market caused by elevated imports in prior years, leading to negative parity between local and international prices.

This suppressed domestic oil prices below import costs, significantly impacting revenues. High inflation and reduced consumer purchasing power adversely affected demand, particularly in bulk commodity segments.

Financial charges more than doubled in FY24 to PKR 7.4 billion, driven by higher borrowing costs amid elevated interest rates. In 1QFY25, financial charges rose by 7% YoY to PKR 1.9 billion. Profit after tax (PAT) turned into a loss of PKR 3.4 billion in FY24 compared to a profit of PKR 675 million in FY23, translating to a net margin of -4%.

The situation was slightly better in 1QFY25, where the company posted a marginal PAT of PKR 88 million compared to a loss of PKR 660 million in 1QFY24, though margins remained subdued. Exports contributed PKR 7.8 billion in FY24, with future emphasis on expanding rice, confectionery, and savory product exports, targeting markets with large ethnic populations.

Distribution networks in the Middle East, UK, and Canada are being strengthened. In edible oil, the company has increased refining capacity by 300 tons/day, enhancing efficiency and cost control. Sales mix has shifted from bulk segment, with a future focus on branded retail oil products. Sunridge flour remains a flagship product, capturing a growing market share in premium branded staples.

Processing capacity for wheat is approximately 940 tons/day, translating to potentially 2.14% of the total market share. Unity Foods has introduced rice under the Sunridge brand, aiming to compete in both local and export markets. Unlike flour, rice faces established competition, but management is leveraging the Sunridge reputation for premium quality. Exports are expected to form a significant part of the rice segment, targeting regions with large ethnic populations.

The management noted that the Palm oil prices are currently steady, with no significant increases expected in the near term. Management noted the impact of the El Niño weather phenomenon, which causes lower rainfall in key palm oil-producing countries like Indonesia and Malaysia. This could potentially affect crop yields but hasn’t yet caused a substantial price surge.

Historically, palm oil prices have closely shadowed petroleum prices. However, this correlation has weakened due to the current weather conditions and supply factors. Going forward, the management aims to revert to FY23 revenue levels (PKR 100 billion) with a higher share of branded and value-added sales. Gross margins are expected to remain steady at FY22-FY23 levels, barring unforeseen market shocks. Plans include further innovation in confectionery, savory snacks, and rice to expand the product portfolio.

Continued emphasis on building a robust export footprint with potential entry into landlocked markets like Azerbaijan and Uzbekistan for processed edible oil. The favorable impact of declining interest rates is expected to materialize from January 2025 onwards.

Important Disclosures

Disclaimer: This report has been prepared by Chase Securities Pakistan (Private) Limited and is provided for information purposes only. Under no circumstances, this is to be used or considered as an offer to sell or solicitation or any offer to buy. While reasonable care has been taken to ensure that the information contained in this report is not untrue or misleading at the time of its publication, Chase Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. From time to time, Chase Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in any transaction, in any securities directly or indirectly subject of this report Chase Securities as a firm may have business relationships, including investment banking relationships with the companies referred to in this report This report is provided only for the information of professional advisers who are expected to make their own investment decisions without undue reliance on this report and Chase Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this report or its contents At the same time, it should be noted that investments in capital markets are also subject to market risks This report may not be reproduced, distributed or published by any recipient for any purpose.